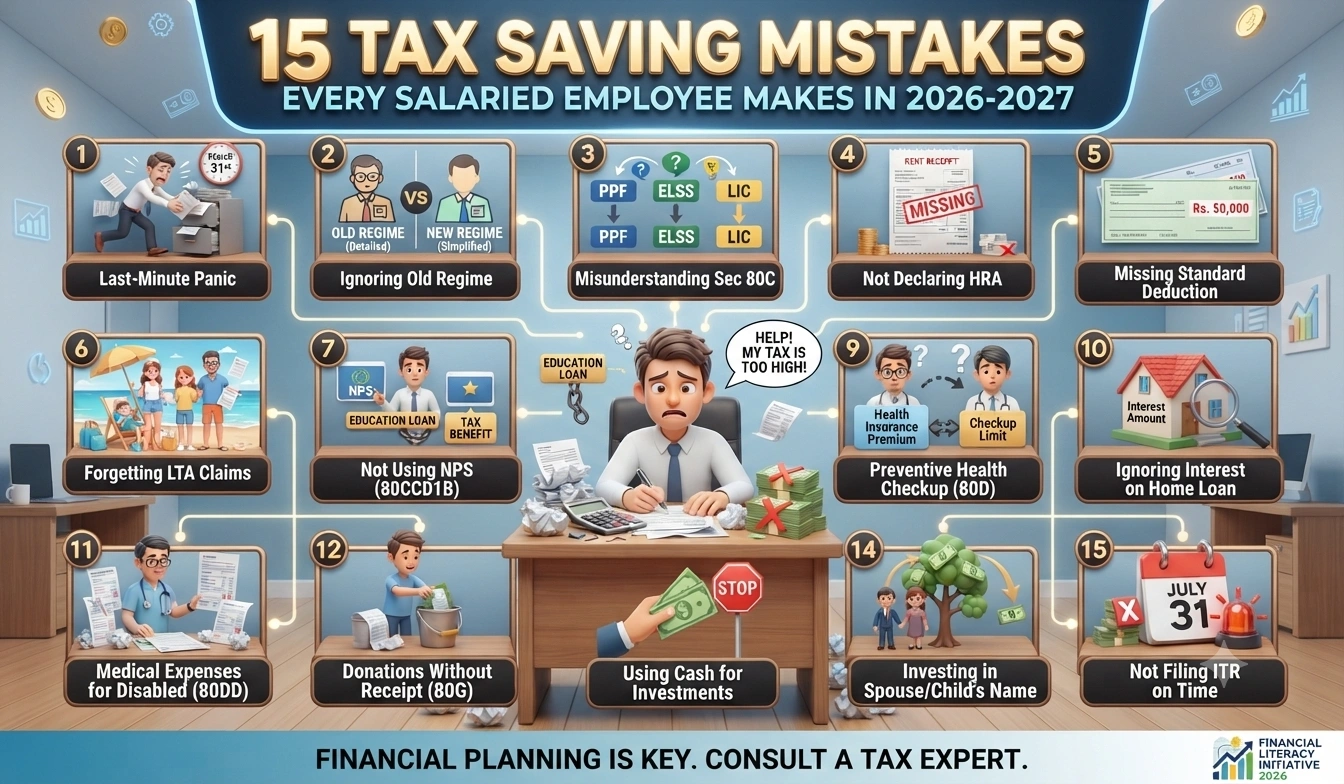

15 Tax Saving Mistakes Every Salaried Employee Makes in 2026-2027

15 Tax Saving Mistakes Every Salaried Employee Makes

Stop leaving money on the table. Here's what you're doing wrong with your taxes.

Look, I've worked with hundreds of salaried employees over the years, and I see the same mistakes repeatedly. You work hard all year, pay your taxes honestly, and then—without realizing it—you miss out on thousands in tax benefits you could've claimed. The worst part? Most of these mistakes are totally avoidable.

So what does this mean for you? It means that by the end of this article, you'll know exactly what you're doing wrong and how to fix it before the 2026-2027 financial year ends. Let me walk you through the 15 biggest tax saving mistakes I see salaried employees make.

1. Not Investing in Section 80C Schemes at All

This is the biggest one. Section 80C lets you save up to ₹1,50,000 per financial year on your taxable income. And yet, I meet people every single day who don't invest a single rupee.

If you earn ₹8 lakh per year and fall in the 30% tax bracket, not investing in 80C costs you ₹45,000 in extra taxes annually. That's real money.

Investing ₹1,50,000 in ELSS mutual funds or PPF saves you between ₹30,000 to ₹45,000 in taxes depending on your slab, plus you get wealth creation on top.

2. Ignoring Section 80D Health Insurance Deductions

And here's another one most people skip. Section 80D gives you deductions for health insurance premiums paid for yourself and your family. If you're self-paying for health insurance, you're literally throwing away tax relief.

For 2026-2027, you can claim up to ₹25,000 for yourself and spouse, and ₹25,000 for parents (or ₹50,000 if parents are senior citizens). That's ₹1,00,000 in deductions if you cover everyone.

- Health insurance for self and spouse: ₹25,000

- Health insurance for parents: ₹25,000

- Senior citizen parents (above 60): ₹50,000

- Preventive health check-up: ₹5,000

But here's the thing: you need proper documentation. Keep your insurance policy copies and premium receipts. Don't just claim it without proof.

3. Missing Home Loan Interest Deductions Under Section 24

If you've taken a home loan, you can claim the entire interest paid as a deduction under Section 24. No limit. But most employees don't claim it properly, or they forget altogether.

Let's say you've paid ₹4 lakh in home loan interest this year. That's ₹4 lakh straight off your taxable income. At 30% tax rate, that's ₹1,20,000 you don't have to pay in taxes.

You need the interest certificate from your bank. Don't claim without it. The income tax department will ask for proof during an audit.

4. Not Claiming Principal Repayment Under Section 80EE

Honestly, this one surprises me. Section 80EE lets you claim up to ₹1,50,000 in principal repayment if you're a first-time home buyer. That's on top of the interest deduction.

So you get interest deduction under 24 plus principal deduction under 80EE. Combined, this can save you massive amounts. But the catch? This only applies if you bought your first home after April 1, 2019, and the property value is up to ₹45 lakh.

Most first-time buyers don't know this exists. Check if you qualify.

5. Forgetting About Education Loan Interest Under Section 80E

If you're still paying back an education loan, Section 80E is your friend. You can claim the entire interest amount—no limit—as a deduction.

The thing is, there's no cap. If you paid ₹2 lakh in interest, you claim ₹2 lakh. For 8 years of repayment, this can add up to massive savings. But you need to file your return to claim it. Skipping your return means losing this benefit forever.

6. Not Filing Your Income Tax Return Even When Not Required

And this is critical. If your income is below the taxable limit, you might think you don't need to file a return. Wrong.

Filing a return even when you don't owe taxes gives you a clear record for banks, loans, visa applications, and business purposes. Plus, if you've paid taxes through TDS, you won't get your refund unless you file.

In 2026-2027, if your employer has deducted tax from your salary but your actual tax liability is lower, you're entitled to a refund. But you won't get it without filing.

7. Ignoring Section 80CCD(1B) NPS Deductions

Section 80CCD(1B) lets you claim an additional ₹50,000 deduction for NPS contributions, over and above the ₹1,50,000 limit under 80C.

So if you're already maxing out 80C, you can push another ₹50,000 into NPS and get that deducted too. That's ₹2,00,000 total deduction from these two sections alone.

Most employees don't know this, so they miss it.

8. Not Claiming Rent Paid Under Section 80GG

If you're paying rent but not claiming it as a deduction, you're missing out. Section 80GG lets you claim rent paid as a deduction if you don't own a house.

The maximum deduction is the least of: (a) ₹5,000 per month (₹60,000 per year), (b) 10% of your gross total income, or (c) actual rent paid minus 10% of gross total income.

If you're paying ₹25,000 rent monthly and earning ₹8 lakh annually, you can claim up to ₹60,000 as deduction. That's ₹18,000 in tax savings at 30% slab.

9. Claiming Deductions Without Proper Documentation

So you know about 80C, 80D, and other deductions. But you're claiming them without keeping proper paperwork. That's a disaster waiting to happen.

During an audit or assessment, the income tax department will ask for proof. If you don't have it, your deduction gets disallowed, and you end up paying back taxes plus penalties.

- Keep bank statements showing investments

- Keep policy documents from insurance companies

- Keep certificates from mutual fund houses

- Keep home loan interest certificates from banks

- Keep rent receipts or lease agreement copies

- Keep medical bills and insurance premium receipts

The income tax department is now matching data from banks and insurance companies. If you claim a deduction without proof, it'll be caught during cross-verification.

10. Not Updating Your Aadhaar-PAN Link

This is a compliance mistake that can cost you. Your Aadhaar and PAN must be linked. If they're not, your return filing gets rejected.

You can link them online through the income tax portal in 2 minutes. Don't delay this.

11. Missing the Deadline for Filing Returns

For the financial year 2026-2027, the return filing deadline is July 31, 2027 (or October 31, 2027 if you're filing a revised return). Missing this deadline means late filing penalties and loss of certain benefits.

Mark your calendar now. Don't wait until the last week.

12. Not Claiming Standard Deduction

Every salaried employee gets a standard deduction of ₹50,000 from their gross salary. But you need to claim it in your return. If you're filing manually, make sure this is included.

Most tax filing software does this automatically, but if you're doing it yourself, don't miss it.

13. Not Reporting All Sources of Income

If you have income from multiple sources—salary, rental income, interest on savings, dividend income—you must report all of it. Hiding income is tax evasion, and it's a serious offense.

The income tax department now has data from banks, brokers, and other financial institutions. They'll catch unreported income during assessment.

14. Investing in Wrong Instruments for Tax Saving

Just because something qualifies for Section 80C doesn't mean it's the right investment for you. I see people buying life insurance policies they don't need just to save taxes.

ELSS mutual funds are usually better than life insurance for tax saving because they have lower lock-in periods (3 years vs 5-15 years) and better returns. PPF is good if you want guaranteed returns. FDs are not ideal for tax saving.

Match your investment to your goal, not just to your tax bracket.

15. Not Reviewing Your Salary Structure for Optimal Tax Planning

And finally, this one's often missed. Your salary structure matters. If your employer offers flexible benefits, you can restructure your salary to save more taxes.

For example, if you're paying for your own health insurance, ask your employer to add it as a benefit component. That amount becomes a deduction under Section 80D, and it's also exempt from tax under Section 10(D).

Similarly, if you're paying for professional development courses, ask for it as a benefit. These small changes can save you ₹20,000 to ₹50,000 annually.

Quick Comparison Table: Common Tax Saving Mistakes and Their Impact

| Mistake | Annual Tax Cost (30% Slab) | 5-Year Impact |

|---|---|---|

| Not investing in 80C (₹1,50,000) | ₹45,000 | ₹2,25,000 |

| Ignoring 80D health insurance (₹60,000) | ₹18,000 | ₹90,000 |

| Missing home loan interest deduction (₹4,00,000) | ₹1,20,000 | ₹6,00,000 |

| Not claiming rent deduction (₹60,000) | ₹18,000 | ₹90,000 |

| Combined impact of all 4 mistakes | ₹2,01,000 | ₹10,05,000 |

Action Plan for 2026-2027: What You Should Do Now

Put simply, here's what you need to do before the financial year ends:

- Invest ₹1,50,000 in 80C (ELSS, PPF, or life insurance)

- Buy or renew health insurance and claim 80D deduction

- Collect all home loan interest certificates from your bank

- If you're an NPS subscriber, contribute additional ₹50,000 for 80CCD(1B)

- Gather all rent receipts if you're claiming 80GG

- Compile all documentation for deductions you're claiming

- Link your Aadhaar with PAN if you haven't already

- File your return before July 31, 2027

Frequently Asked Questions

Q1: Can I claim deductions for investments made after March 31, 2027?

No. For the financial year 2026-2027, all investments must be made before March 31, 2027. Anything after that goes into the next financial year's return.

Q2: What happens if I don't have receipts for my 80C investments?

You won't be able to claim the deduction during an audit. The income tax department will disallow it. Always keep investment proofs, bank statements, and policy documents.

Q3: Can I claim both 80C and 80CCD(1B) for NPS?

Yes, but with limits. Up to ₹1,50,000 of NPS contributions can be claimed under 80C. Any additional amount (up to ₹50,000) can be claimed under 80CCD(1B). So maximum NPS deduction is ₹2,00,000.

Q4: What's the deadline for filing my 2026-2027 return?

July 31, 2027 is the normal deadline. If you're filing a revised return, the deadline is October 31, 2027. Don't miss these dates—penalties apply if you file late.

Q5: Do I need to file a return if my income is below the taxable limit?

Technically no, but you should. Filing gives you a clear record for loans, visas, and business purposes. Plus, if your employer deducted tax, you won't get your refund without filing a return.

Q6: Can I claim rent deduction if I own a house but don't live in it?

No. Section 80GG specifically says you can't own a house. If you own property anywhere, you're not eligible for this deduction, even if you're renting somewhere else.

The Bottom Line

Tax saving isn't complicated. But it does require attention to detail and proper planning. The 15 mistakes I've outlined here cost salaried employees crores of rupees every year.

The good news? Every single one of these mistakes is preventable. Start now. Review your current investments, check your documentation, and make sure you're not leaving money on the table.

And honestly, if you're unsure about anything, talk to a CA. A 1-hour consultation can save you ₹50,000 in taxes. That's a no-brainer investment.

" } ```

© 2026 Tax Esquire | Expert CA Services in Greater Noida, Uttar Pradesh

8810380146 | info.taxesquire@gmail.com | taxesquire.in

This document is for informational purposes only. For personalised tax advice, consult our chartered accountants.