Complete Guide For Income Tax Deductions for Self-Employed Professionals in India 2026-2027

Income Tax Deductions for Self-Employed Professionals in India 2026-2027

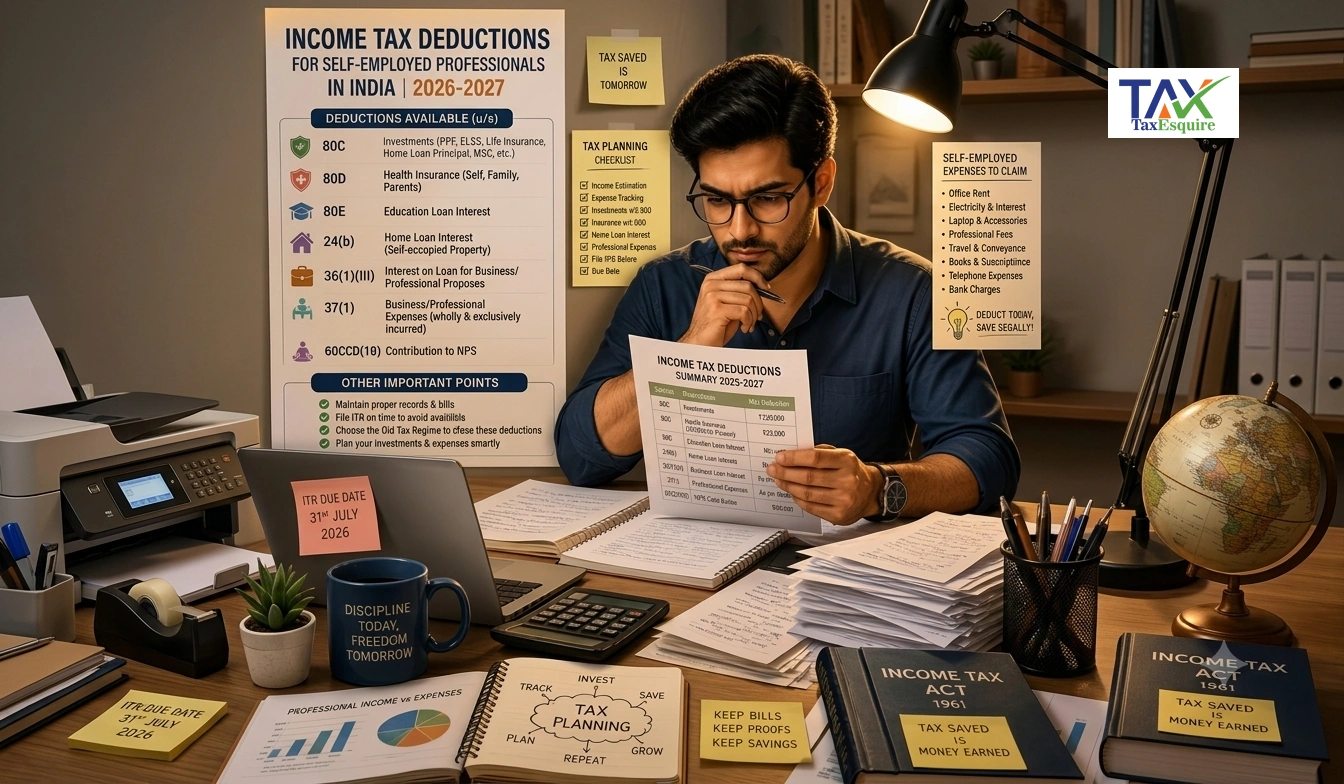

Master every tax deduction available to you as a self-employed professional and save money legally

Why Self-Employed Professionals Need to Know About Tax Deductions

Look, if you're self-employed in India, you're probably paying more tax than you need to. And that's not because you're doing anything wrong—it's because most professionals simply don't know what they can actually deduct.

The thing is, the Income Tax Act gives you plenty of room to reduce your taxable income. But here's what I see all the time: freelancers, consultants, and business owners leave money on the table because they're not tracking the right expenses. So what does this mean for you? It means you could be paying thousands of rupees more than you should.

In 2026-27, the rules haven't changed much, but the opportunities are still massive. Put simply, every rupee you can legitimately deduct is a rupee you don't pay tax on. That's not tax evasion—that's smart tax planning.

Proper deduction planning can reduce your effective tax rate by 15-25% depending on your income level and business structure.

Understanding Section 44ADA and Section 44AA

Before we talk about specific deductions, you need to understand the basic framework. There are two main regimes for self-employed professionals in India: the regular method and the presumptive income method.

Under Section 44ADA, if you're a professional (doctor, lawyer, CA, consultant, etc.), you can claim deductions up to 50% of your gross professional income. This is huge. And honestly, most professionals don't use this properly.

Section 44AA applies to non-professionals like traders and manufacturers. Here, you can claim deductions up to 40% of gross turnover. The benefit of these sections is that you don't need to maintain detailed books—you just claim the prescribed percentage.

| Category | Applicable Section | Deduction % | Applies To |

|---|---|---|---|

| Professionals | Section 44ADA | 50% | Doctors, lawyers, consultants, CAs |

| Non-Professionals | Section 44AA | 40% | Traders, manufacturers, shopkeepers |

| Actual Method | Regular books | Actual expenses | All self-employed persons |

You can't use both the presumptive method and claim actual deductions. Pick one method and stick with it for the entire financial year. Switching between methods can invite scrutiny from the tax authorities.

Major Deductions You Can Claim as Self-Employed

And now let's get into the real stuff. Here are the deductions you can actually claim if you're self-employed in 2026-27:

1. Office and Business Premises Rent

If you work from a rented office, the entire rent is deductible. But here's the catch: if you rent from a family member, you need to show that the rent is at market rate and that you've actually paid it. The income tax department doesn't like artificial deductions.

Let me give you an example. Rahul is a consultant who rents a 1000 sq ft office for Rs 30,000 per month. That's Rs 3,60,000 per year—fully deductible. But if Rahul rents from his father for Rs 5,000 per month when market rate is Rs 30,000, the department will disallow the deduction or allow only the market rate amount.

- Rent for office space, clinic, workshop, or studio

- Rent for equipment storage

- Rent for client meeting spaces

- Parking charges for business vehicles

- Common area maintenance charges (if separate)

2. Utilities and Office Running Costs

Basically, any cost to keep your office running is deductible. This includes electricity bills, water charges, internet, phone bills, and office supplies.

But—and this is important—if you work from home, you can only deduct the portion that relates to your office. You can't deduct 100% of your home electricity bill. The general rule is to deduct the percentage of your office space compared to your total home area.

- Electricity and water bills

- Internet and phone charges

- Stationery and office supplies

- Postage and courier charges

- Office furniture and equipment repairs

3. Professional Fees and Licenses

Any fee you pay to maintain your professional status is fully deductible. This includes professional association fees, license renewal charges, and statutory compliance costs.

For example, if you're a CA, your ICAI membership fees, continuing professional education charges, and practicing certificate renewal are all deductible. Same goes for doctors, lawyers, and other regulated professionals.

4. Travel and Client Meeting Expenses

Any travel for business purposes is deductible. This includes cab fares, flights, trains, and hotels when you're traveling for client work or business development.

The thing is, you need to keep proper documentation. Maintain a travel log showing the date, destination, purpose, and amount. The income tax department won't accept vague claims like "business travel" without details.

Here's a practical example: Priya is a management consultant. She travels to Mumbai for 3 days to meet a client. Flight ticket: Rs 8,000. Hotel: Rs 5,000 per night (Rs 15,000 total). Meals and local transport: Rs 3,000. Total deductible: Rs 26,000. All of it is allowed because it's directly for business purposes.

- Flight and train tickets for business travel

- Hotel accommodation during business trips

- Taxi and cab fares for client meetings

- Meals during business travel

- Vehicle fuel for business purposes

- Parking and toll charges

5. Employee Salaries and Contractor Payments

If you have employees or hire contractors, their salaries and fees are fully deductible. But here's what matters: you must deduct TDS (Tax Deducted at Source) from contractor payments above Rs 30,000 per month.

And that's really it—pay the salary, deduct TDS where required, file TDS returns on time, and you're good. But if you don't deduct TDS when you should, the entire payment becomes disallowed.

6. Depreciation on Equipment and Assets

When you buy equipment, furniture, or tools for your business, you can claim depreciation each year instead of deducting the full amount upfront. The depreciation rates vary by asset type.

For instance, if a consultant buys a laptop for Rs 1,00,000, they can't deduct the full amount in year one. Instead, they claim depreciation at 40% per year on the written-down value. Year 1 depreciation: Rs 40,000. Year 2: Rs 24,000 (40% of Rs 60,000). And so on.

| Asset Type | Depreciation Rate | Notes |

|---|---|---|

| Computers and laptops | 40% | Written-down value method |

| Office furniture | 10% | Written-down value method |

| Vehicles | 15% | Written-down value method |

| Medical equipment | 40% | Varies by equipment type |

7. Professional Indemnity and Business Insurance

Any insurance premium you pay for your business is deductible. This includes professional indemnity insurance, general liability insurance, and business interruption insurance.

Health insurance premiums for yourself and your employees are also deductible. But—and this is a big but—personal life insurance isn't deductible, even if you're self-employed.

8. Interest on Business Loans

If you've taken a loan to start or expand your business, the interest portion is fully deductible. The principal repayment isn't deductible, but the interest is.

Let's say you took a Rs 5,00,000 business loan at 10% per year. Year 1 interest: Rs 50,000. That's fully deductible. The principal repayment isn't, but you get the interest deduction.

9. Advertising and Marketing Expenses

Any money you spend to promote your business is deductible. This includes website development, social media advertising, business cards, brochures, and professional photography.

But here's the thing: the expense must be for business promotion, not personal benefit. You can't deduct the cost of a fancy personal photoshoot just because you use one photo on your website.

10. Professional Development and Training

Courses, certifications, workshops, and training programs that improve your professional skills are deductible. This is huge for self-employed professionals who need to stay updated.

If you're a digital marketer and you take a course on AI-powered marketing for Rs 15,000, that's fully deductible. Same goes for any professional development that directly relates to your business.

What You Can't Deduct (Common Mistakes)

So what can't you deduct? Let me be clear about this because I see people make these mistakes all the time.

- Personal expenses (groceries, personal clothing, personal entertainment)

- Capital expenditures (you depreciate these instead, not deduct fully)

- Income tax and penalties paid to the government

- Personal life insurance premiums

- Home loan principal repayment (interest is deductible, not principal)

- Fines and penalties for breaking laws

Don't try to be clever. The tax department has data analytics tools that flag unusual deduction patterns. If your deductions are way higher than industry averages, you'll get an audit notice. Keep your deductions reasonable and well-documented.

Documentation and Record-Keeping Requirements

Here's the reality: deductions are only as good as your documentation. The tax department won't believe you without proof.

For every deduction you claim, you need to maintain supporting documents. This includes invoices, receipts, bank statements, bills, and contracts. Keep these records for at least 6 years—that's the statute of limitations for tax assessments.

And that's really important: digital records are now accepted. You don't need physical copies anymore. Use accounting software, maintain digital invoices, and keep PDF copies of all bills.

- Original invoices and receipts for all expenses

- Bank statements showing payments

- Travel logs and expense sheets for business travel

- Contracts and agreements with clients and vendors

- Utility bills showing business premises

- TDS certificates for contractor payments

- Asset purchase invoices and depreciation schedules

Using accounting software like Tally, Busy, or cloud-based solutions helps you maintain organized records automatically. This reduces the chance of missing deductions and makes audit defense much easier.

Practical Example: Calculating Deductions for Different Professionals

Example 1: Freelance Consultant (Using Presumptive Method)

Amit is a management consultant with gross professional income of Rs 30,00,000 in FY 2026-27. He qualifies for Section 44ADA (professional income up to Rs 50 lakhs).

Using the presumptive method, he can claim deductions up to 50% of gross income = Rs 15,00,000. So his net taxable income is Rs 15,00,000. At 30% slab rate (plus cess), his tax liability is about Rs 4,65,000. Without this deduction, he'd pay nearly Rs 9,30,000. That's a saving of Rs 4,65,000 annually.

Example 2: Medical Practitioner (Using Actual Method)

Dr. Sharma runs a clinic with gross income of Rs 40,00,000 in FY 2026-27. She maintains detailed books and claims actual deductions:

- Clinic rent: Rs 2,00,000

- Staff salaries: Rs 12,00,000

- Equipment depreciation: Rs 1,50,000

- Utilities and supplies: Rs 3,00,000

- Professional insurance: Rs 50,000

- Continuing education: Rs 1,00,000

- Other expenses: Rs 2,00,000

Total deductions: Rs 22,00,000. Taxable income: Rs 18,00,000. Tax liability: about Rs 5,40,000. If she had used the presumptive method, she'd only get 50% deduction = Rs 20,00,000 taxable income, leading to higher tax. So the actual method is better here.

Tax Planning Tips for Self-Employed Professionals in 2026-27

And now for the practical stuff. Here's how to actually reduce your tax burden legally:

- Track all business expenses in real-time. Don't wait until March 31 to gather receipts.

- Invest in Section 80C instruments (life insurance, PPF, ELSS) to get additional deductions up to Rs 1,50,000.

- Consider health insurance under Section 80D. You can deduct up to Rs 25,000 for yourself and Rs 50,000 if you're 60 years or older.

- If you have home office expenses, maintain a separate utility bill or calculate the proportionate share of your home expenses.

- Don't mix personal and business expenses. Keep separate bank accounts and credit cards for business.

- Claim depreciation on all assets. Many professionals forget this and leave money on the table.

Frequently Asked Questions

Q1: Can I deduct my home office rent if I own my home?

No, you can't deduct rent if you own the property. But you can claim depreciation on the building (at 5% per year) and deduct the proportionate share of utilities, internet, and maintenance. If your home is Rs 50 lakhs and you use 20% for office, you can claim 20% depreciation annually.

Q2: What's the difference between Section 44ADA and actual method?

Section 44ADA is simpler—you just claim 50% of gross income as deduction without needing to prove actual expenses. The actual method requires you to maintain detailed books and claim only real expenses. Choose the actual method only if your actual expenses are more than 50% of income. Otherwise, stick with Section 44ADA.

Q3: Can I deduct my vehicle loan interest?

Yes, if the vehicle is used exclusively for business. If it's a personal vehicle that you sometimes use for business, you can only deduct the interest proportionate to business use. If you use the vehicle 60% for business and 40% for personal, you can deduct 60% of the interest.

Q4: Am I allowed to deduct meals and entertainment expenses?

Meals during business travel are deductible. But entertainment expenses (like taking clients to movies or shows) are generally not deductible unless they're directly related to business development and you maintain detailed records showing the business purpose and attendees.

Q5: What if I made a mistake in deductions in the previous year?

You can file a revised return within 2 years of the original return date. If the department notices an error, they'll issue a notice. Don't ignore it—respond promptly with proper documentation. Honesty and proper documentation go a long way in resolving tax disputes.

Common Audit Red Flags to Avoid

The thing is, not all deductions are created equal. Some raise more flags than others. Here's what the tax department looks at:

- Deductions that are 70%+ of gross income (unless you have solid documentation)

- Round-number deductions (like exactly Rs 1,00,000 every month)

- Travel expenses that seem excessive for your industry

- Payments to family members without proper documentation

- Cash payments without invoices or receipts

- Deductions that don't match your industry's average expense patterns

If you're selected for a tax audit, the department will scrutinize every deduction. They'll ask for original invoices, bank statements, and explanations. If you can't produce documentation, the deduction gets disallowed and you'll have to pay interest and penalties. So don't claim anything you can't justify.

Wrapping Up: Your Action Plan for 2026-27

So here's what you need to do right now. First, determine whether Section 44ADA or the actual method is better for you. If your actual expenses are less than 50% of gross income, stick with Section 44ADA. Otherwise, go with the actual method.

Second, set up a system to track expenses. Use accounting software. Maintain digital copies of all invoices and receipts. Create a travel log. Separate your business and personal finances completely.

Third, review this guide once more and identify which deductions apply to you. Calculate your potential tax savings. Then work backwards to see how much you need to spend to get those deductions (if you're not already spending that much).

And finally, consider consulting a CA who specializes in self-employed taxation. The fee you pay for professional advice will be way less than the tax you'll save.

Proper tax planning can easily save you Rs 50,000 to Rs 5,00,000+ annually depending on your income level. That's money you get to keep instead of paying to the government.

" } ```

© 2026 Tax Esquire | Expert CA Services in Greater Noida, Uttar Pradesh

8810380146 | info.taxesquire@gmail.com | taxesquire.in

This document is for informational purposes only. For personalised tax advice, consult our chartered accountants.