Rates of Depreciation as Per Companies Act, 2013: Complete Guide for Indian Businesses

Rates of Depreciation as Per Companies Act, 2013

Your complete roadmap to understanding asset depreciation, compliance, and practical implementation

What is Depreciation Under Companies Act, 2013?

Depreciation is the systematic reduction in the value of a fixed asset over its useful life. When you buy a machine, building, or vehicle for your business, it doesn't retain its full value forever. The Companies Act, 2013 recognizes this reality and gives you a framework to account for it properly.

But here's the thing—depreciation isn't just an accounting concept. It's a legal requirement. Schedule II of the Companies Act, 2013 lays down specific rates you must follow. Miss these, and your financial statements won't comply with the law.

So what does this mean for you? Whether you're running a manufacturing unit, a trading business, or a service firm, you need to get depreciation right. And that's really it—get it right from day one, and your auditor will be happy.

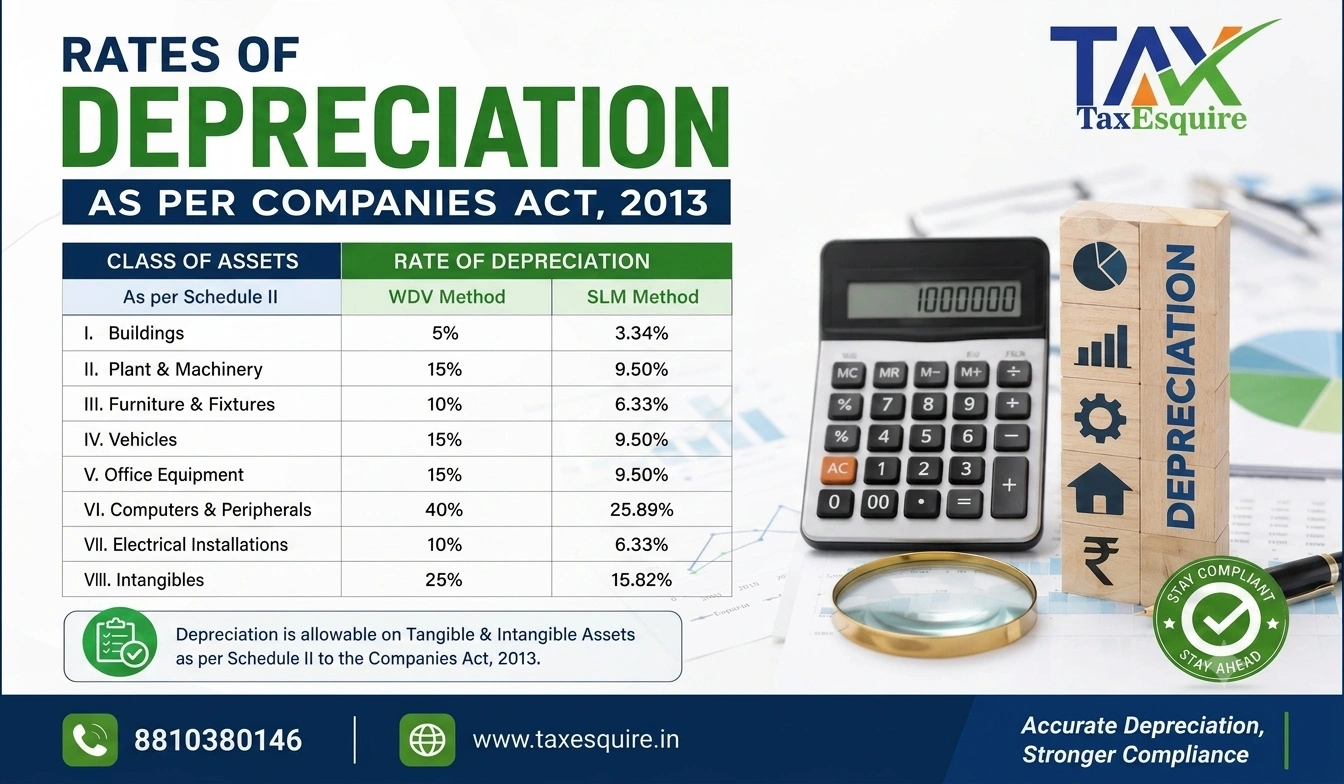

Schedule II: The Legal Framework

Schedule II of the Companies Act, 2013 is your bible for depreciation. It lists different categories of assets and their corresponding depreciation rates. These aren't suggestions—they're compulsory.

The rates are expressed as percentages per annum on the original cost of the asset. And here's what makes it interesting: the rates vary significantly depending on the nature of the asset. A building depreciates slowly. A computer depreciates fast. Why? Because that's how long they last in real business life.

The law gives you flexibility in one way, though. You can choose between the Straight Line Method (SLM) and the Written Down Value Method (WDV). Put simply, SLM depreciates the same amount every year. WDV depreciates more in early years and less later.

Following Schedule II rates ensures your financial statements are compliant with the law. This protects you during audits, GST compliance checks, and any regulatory scrutiny.

Major Asset Categories and Their Depreciation Rates

Let me walk you through the main categories. These are the assets most businesses deal with, and the rates that apply to them.

| Asset Category | Depreciation Rate (SLM) | Useful Life (Years) |

|---|---|---|

| Buildings (RCC) | 3.34% | 30 |

| Plant and Machinery | 4.75% to 15% | 20 to 7 |

| Furniture and Fittings | 10% | 10 |

| Motor Vehicles | 9.5% to 14.29% | 7 to 10 |

| Computers and IT Equipment | 20% | 5 |

| Office Equipment | 10% | 10 |

Notice how computers depreciate at 20% per year? That's because technology becomes outdated quickly. A building, on the other hand, depreciates at just 3.34% because it lasts for 30 years.

Straight Line Method vs. Written Down Value Method

You get to pick one. But you can't switch between them casually. Once you choose, stick with it for that asset class.

The Straight Line Method (SLM) divides the cost equally across all years. Say you buy a machine for ₹1,00,000 with a 10-year life. You depreciate ₹10,000 every year. Simple. Predictable. Most small businesses use this.

The Written Down Value Method (WDV) applies the rate to the remaining book value each year. So in year one, you depreciate ₹10,000 on ₹1,00,000. In year two, you depreciate the rate on ₹90,000. The depreciation amount gets smaller each year. But here's why some prefer it: it matches how assets actually lose value in the real world.

And that's the key difference. WDV is more realistic for tax purposes, which is why income tax law prefers it. But Companies Act allows both for book purposes.

Don't mix methods for the same asset class. If you use SLM for one machine, use it for all machines. Mixing creates audit nightmares and compliance issues.

Practical Examples: How Depreciation Works

Let me give you real scenarios. These are the kind of situations you'll actually face in 2026 and 2027.

Example 1: Manufacturing Unit Buys Plant and Machinery

A small manufacturing unit buys a lathe machine for ₹5,00,000 on 1st April 2026. The useful life is 10 years. The depreciation rate under Schedule II is 10% per annum under SLM.

Depreciation for 2026-27 = ₹5,00,000 × 10% = ₹50,000. That's what goes into your P&L statement. The machine's book value on 31st March 2027 becomes ₹4,50,000.

Example 2: IT Company Buys Computers

An IT firm buys 10 computers for ₹5,00,000 total on 1st July 2026. Computers depreciate at 20% per annum. But since it's purchased mid-year, you depreciate for 9 months only (1st July to 31st March 2027).

Depreciation = ₹5,00,000 × 20% × (9/12) = ₹75,000. This is crucial—you don't depreciate for the full year if the asset is acquired mid-year.

Example 3: Office Building Purchased

A trading company buys an office building for ₹20,00,000 on 1st April 2026. Buildings depreciate at 3.34% per annum. Annual depreciation = ₹20,00,000 × 3.34% = ₹66,800. That's what you expense every year for 30 years.

Assets That Don't Depreciate

Not everything depreciates. Land is the classic example. It doesn't wear out. So you never depreciate land. But you do depreciate the building standing on it.

Here's what else doesn't depreciate:

- Land (any type)

- Leasehold land improvements (they follow different rules)

- Assets held for sale (these are current assets, not fixed)

- Intangible assets like goodwill and patents (they follow amortization rules, not depreciation)

- Investments in subsidiaries or associates

So when you're classifying assets, separate land from the building. Your accountant will thank you.

Depreciation and Tax Compliance

Here's where it gets interesting. Book depreciation under Companies Act isn't the same as tax depreciation under the Income Tax Act.

For books, you follow Schedule II. For taxes, you follow Section 32 of the Income Tax Act. These rates are different. So you might depreciate ₹50,000 in your books but claim ₹60,000 as a tax deduction. The difference becomes a timing difference in your deferred tax calculation.

And that's really important. Your auditor will check that you've reconciled book depreciation with tax depreciation in the notes to accounts. If you haven't, it's a compliance failure.

Understanding the difference between book and tax depreciation helps you manage your tax liability better. You can plan asset purchases strategically to optimize your tax position while staying compliant.

Common Depreciation Mistakes to Avoid

I've seen businesses mess up depreciation in ways that create serious problems. Let me share the most common ones.

Mistake 1: Depreciating Land

Some businesses buy a property for ₹50,00,000 and depreciate the entire amount. Wrong. You need to segregate land from the building. If the land is ₹20,00,000 and the building is ₹30,00,000, only depreciate the building.

Mistake 2: Applying Wrong Rates

You buy machinery and depreciate it at 10%. But Schedule II says it should be 15%. Your financial statements are now non-compliant. This gets caught in audit.

Mistake 3: Inconsistent Application

You use SLM for some assets and WDV for others in the same class. This violates accounting standards and creates audit queries.

Mistake 4: Full Year Depreciation for Mid-Year Purchases

You buy a computer on 1st December 2026 and depreciate it for the full year. But it should be depreciated for 4 months only (December to March). This overstates your depreciation expense.

Mistake 5: Forgetting Salvage Value

Some assets have salvage value. If you buy a vehicle for ₹10,00,000 and it'll be worth ₹2,00,000 at the end, you depreciate only ₹8,00,000. Ignoring this overstates depreciation.

Depreciation mistakes often go unnoticed until audit time. Then you're stuck making adjustments that create additional tax liability and penalties. Get it right from day one.

Depreciation Disclosure Requirements

Your financial statements aren't complete if you don't disclose depreciation properly. Schedule II requires specific disclosures.

You need to show:

- Gross block of each asset category

- Accumulated depreciation

- Net book value

- Depreciation method used

- Useful life assumptions

- Depreciation rates applied

- Movements during the year (additions, disposals, transfers)

This is usually presented in a note to the balance sheet. If you're using accounting software, it should generate this automatically. If you're doing it manually, be very careful with the calculations.

Depreciation for Different Business Types

Different businesses have different asset mixes. Let me break it down.

Manufacturing Businesses

You have heavy machinery, buildings, and vehicles. Machinery rates vary from 4.75% to 15% depending on type. Buildings are 3.34%. Your biggest depreciation expense usually comes from machinery.

Retail and Trading Businesses

You have shop fittings, display equipment, cash registers, and vehicles. Fittings depreciate at 10%, vehicles at 9.5% to 14.29%. Your depreciation is usually moderate.

IT and Software Companies

You have computers, servers, and office equipment. Computers depreciate at 20%, which is quite high. Over 5 years, your entire computer fleet becomes fully depreciated. Plan accordingly.

Real Estate Companies

You have buildings and land. Buildings depreciate at 3.34%, land doesn't. Your depreciation is low but consistent for 30 years.

Frequently Asked Questions

Q1: Can I depreciate an asset below its salvage value?

No. If an asset has a salvage value of ₹2,00,000, you can't depreciate it below that. You depreciate only the depreciable base, which is cost minus salvage value.

Q2: What happens if I buy an asset mid-year?

You depreciate it for the number of months you own it. If you buy on 1st October 2026, you depreciate for 6 months in that year (October to March). This is called pro-rata depreciation.

Q3: Can I change depreciation rates after I've started?

Only if there's a change in the asset's useful life or if there's an impairment. You can't change rates casually. Any change needs disclosure and justification in the notes to accounts.

Q4: Are there any assets with zero depreciation?

Yes. Land, investments, and intangible assets like goodwill don't depreciate. They're either held at cost or tested for impairment.

Q5: What's the difference between depreciation and amortization?

Depreciation applies to tangible assets like buildings and machinery. Amortization applies to intangible assets like software licenses and patents. The concept is the same—spreading cost over useful life—but the terminology differs.

Q6: How do I handle depreciation for assets purchased on lease?

Under Ind AS 116 (which most companies now follow), leased assets are recognized on the balance sheet. You depreciate the right-of-use asset over the lease term. It's different from operating leases under the old rules.

Staying Compliant in 2026-2027

Here's what you need to do right now to ensure compliance for 2026-27:

First, audit your fixed asset register. Verify that every asset is classified correctly. Check that the depreciation rates match Schedule II. If there are discrepancies, correct them before year-end.

Second, document your depreciation policy. Write down which method you're using (SLM or WDV), useful lives, salvage values, and any assumptions. This becomes part of your financial statement notes.

Third, reconcile book depreciation with tax depreciation. Prepare a schedule showing the differences. Your CA will need this for the tax return.

Fourth, use accounting software that tracks depreciation automatically. Manual calculations are error-prone and time-consuming. Modern ERPs handle this seamlessly.

Proper depreciation management improves your financial reporting quality, makes audits smoother, and ensures you're not overpaying or underpaying taxes.

Conclusion

Depreciation under the Companies Act, 2013 isn't complicated once you understand the basics. Schedule II gives you clear rates. You pick a method. You apply it consistently. And you disclose everything properly.

The key is getting it right from the start. Depreciation mistakes compound year after year. What seems like a small error in year one becomes a big headache in year five when you're trying to correct it.

If you're unsure about any asset classification or rate, talk to your CA. It's worth spending an hour getting clarity than spending weeks fixing audit issues later. Your financial statements are the foundation of your business's credibility. Make sure they're built on solid ground.

© 2026 Tax Esquire | Expert CA Services in Greater Noida, Uttar Pradesh

8810380146 | info.taxesquire@gmail.com | taxesquire.in

This document is for informational purposes only. For personalised tax advice, consult our chartered accountants.