Auditing Requirements of Private Limited Company in India

Introduction

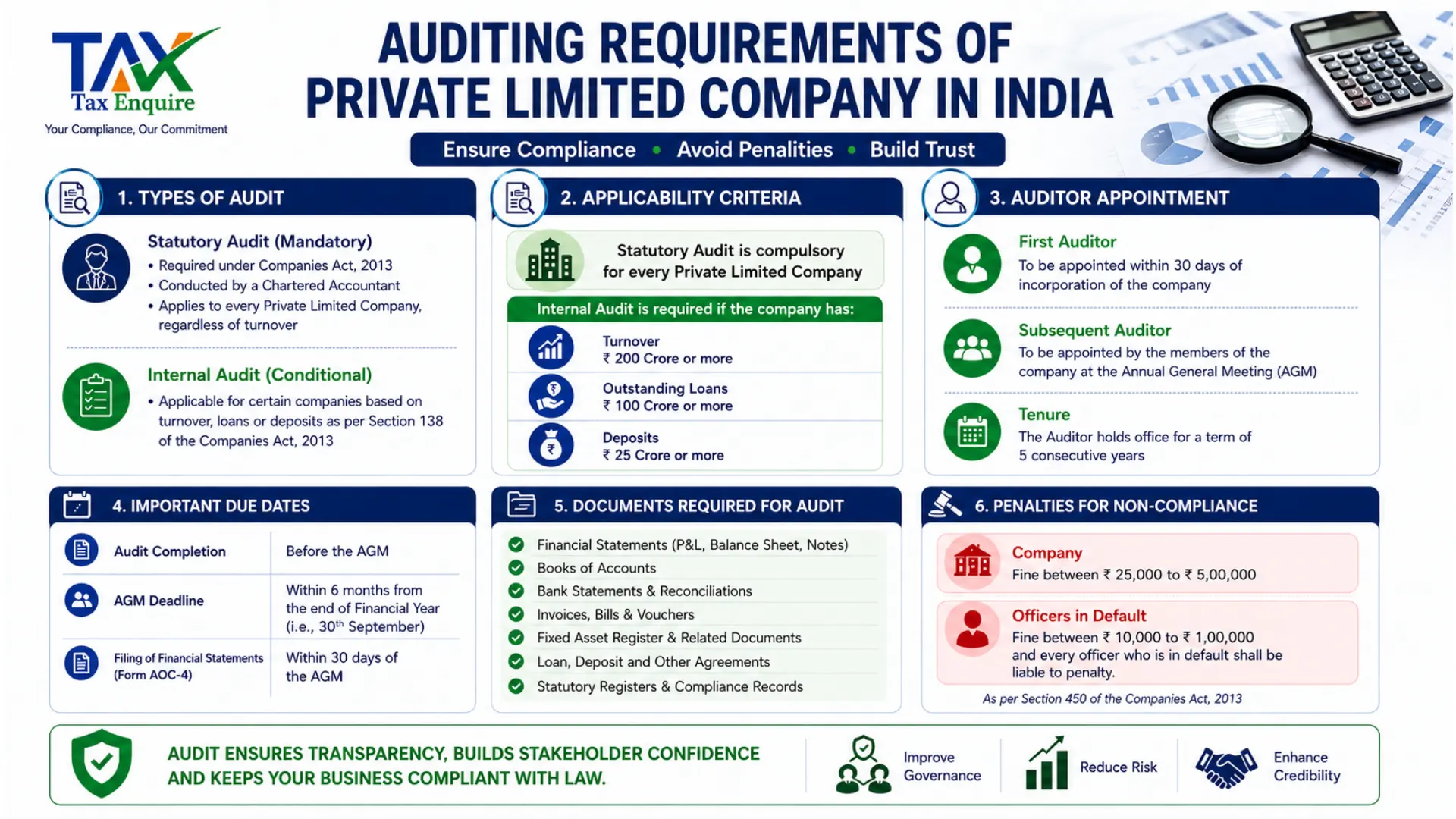

Audit compliance is one of the most critical legal obligations for companies registered in India. Under the Companies Act, 2013, every private limited company is required to maintain proper books of accounts and get them audited annually by a qualified Chartered Accountant.

Unlike sole proprietorship’s or partnership’s, where audit’s applicability depends on turnover, companies are mandatorily subject to statutory audit regardless of size’s, revenue’s, or operational activity. Even dormant companies must comply.

A company audit is an independent and systematic examination of financials statement’s, accounting record’s, and internal control’s of a business.

It is conducted by an independent CA who expresses an opinion on whether the financial statements present a true and fair view of the company’s financial position.

Why Every Private Limited Company Must Conduct an Audit?

An audit is an independent examination of a company’s financial statements, books of accounts, and internal financial controls to verify whether the records are accurate and compliant with applicable laws. It is conducted by a qualified Chartered Accountant who reviews the company’s financial activities and provides an opinion on whether the financial statements present a true and fair view of the company’s financial position.

Under the Companies Act, 2013, every Private Limited Company in India is required to conduct a statutory audit every financial year, irrespective of its turnover, profit, or business activity. Even companies with no transactions or inactive operations must comply with audit requirements.

Types of Audits Applicable to Private Limited Companies

A Private Limited Company in India may be required to undergo different types of audits based on its turnover, business activities, borrowings, and legal requirements. These audits help maintain financial transparency, improve internal controls, and ensure compliance with various laws.

1. Statutory Audit A Statutory Audit is compulsory for every Private Limited Company under Sections 139 and 143 of the Companies Act, 2013, irrespective of turnover or profit. The audit is conducted by a Chartered Accountant to verify whether the company’s financial statements present a true and fair view of its financial position and comply with accounting standards and legal provisions. 2. Internal Audit Internal Audit is applicable to certain companies as prescribed under Rule 13 of the Companies (Accounts) Rules, 2014. It generally applies where turnover exceeds ₹200 crore or outstanding borrowings are more than ₹100 crore. This audit evaluates internal controls, risk management systems, and operational efficiency to strengthen business processes. 3. Cost Audit Cost Audit is required for companies engaged in specified manufacturing or service sectors covered under the Cost Records and Audit Rules. As per Section 148 of the Companies Act, 2013, companies operating in industries such as telecom, power, pharmaceuticals, and manufacturing may need to maintain cost records and conduct a cost audit if the prescribed turnover limits are crossed. The audit ensures proper cost accounting and transparency in pricing structures. 4. Tax Audit Tax Audit is governed by Section 44AB of the Income Tax Act, 1961. It becomes mandatory when the business turnover exceeds ₹1 crore, or ₹10 crore where at least 95% of transactions are carried out digitally. The objective of this audit is to verify the correctness of income, deductions, and tax compliance maintained by the company. 5. Other Applicable Audits Certain companies may also be subject to additional audits depending on their nature and regulatory requirements. Secretarial Audit: Mandatory mainly for listed companies and specified classes of companies under the Companies Act to ensure compliance with corporate laws and governance standards. GST Compliance Review: Although GST Audit was removed from FY 2020–21 onwards, businesses with turnover exceeding ₹5 crore are still required to file GSTR-9C reconciliation statements to confirm the accuracy of GST filings and records. These audits collectively help Private Limited Companies maintain legal compliance, financial discipline, and operational transparency. Appointment of Auditor in a Private Limited Company Under the Companies Act, 2013, only a practicing Chartered Accountant (CA) or a CA firm with a valid Certificate of Practice can be appointed as a company auditor. The auditor must remain independent and should not be a director, employee, or person having a financial interest in the company. Timeline for Auditor Appointment The Board of Directors must appoint the first auditor within 30 days from the date of incorporation. If the Board fails to appoint, shareholders must appoint the auditor within 90 days through an Extraordinary General Meeting (EGM). Subsequent auditors are appointed by shareholders at the Annual General Meeting (AGM) for a term of up to five years. Procedure for Appointment The appointment process generally includes: Passing a Board Resolution for auditor appointment Obtaining written consent and eligibility certificate from the auditor under Section 141 Filing Form ADT-1 with the Registrar of Companies (ROC) within 15 days of appointment. Timely appointment of an auditor ensures legal compliance, strengthens financial transparency, and helps the company avoid future regulatory issues and penalties. How Does the Audit Process Work for a Private Limited Company? The audit process for a Private Limited Company follows a step-by-step procedure to ensure proper financial reporting and compliance with the Companies Act, 2013. 1. Appointment of Auditor The company appoints a Chartered Accountant or audit firm as its auditor and files Form ADT-1 with the Registrar of Companies (ROC) within 15days. 2. Audit Planning The auditor studies the company’s business operations, accounting system, and financial records to understand the scope of the audit. 3. Collection of Documents The company provides important documents such as: Financial statements Bank statements Invoices and bills Accounting records Tax and GST returns 4. Verification and Review The auditor checks financial transactions, verifies records, and reviews internal controls to ensure accuracy and compliance. 5. Preparation of Audit Report After examination, the auditor issues an audit report stating whether the company’s financial statements show a true and fair view of its financial position. 6. ROC Filing and Compliance Finally, the company files audited financial statements and annual compliance forms with the ROC within the prescribed due dates. A proper audit process helps maintain transparency, improves financial discipline, and ensures legal compliance for the company. Important Audit and Filing Timelines for Private Limited Companies Every Private Limited Company must complete its audit and ROC filings within the prescribed deadlines to avoid penalties and maintain legal compliance under the Companies Act, 2013. Key Compliance Timelines Statutory Audit Completion: The annual audit should generally be completed by 30th September for companies following the April–March financial year. Board Approval of Financial Statements: The Board of Directors must approve the audited financial statements before filing them with the Registrar of Companies (ROC). Annual General Meeting (AGM): The AGM must be held within 6 months from the end of the financial year, usually by 30th September, for adoption of audited accounts and appointment or reappointment of auditors. Income Tax Audit (if applicable): Companies covered under Section 44AB of the Income Tax Act must file the tax audit report in Form 3CA/3CB and 3CD by 30th September each year. Important ROC Filing Forms Form AOC-4: Filed within 30 days of the AGM for submission of audited financial statements. Form MGT-7: Filed within 60 days of the AGM for filing the annual return. Form ADT-1: Filed within 15 days of appointment or reappointment of the auditor. Timely completion of audits and ROC filings helps companies avoid late fees, penalties, and legal issues while maintaining an active and compliant business status. Important ROC Forms Form ADT-1: Form AOC-4: Form MGT-7 / MGT-7A: Form 3CA / 3CB and 3CD: Proper documentation is the backbone of a successful audit. Financial Statements: Balance Sheet Profit & Loss Account Cash Flow Statement Supporting Documents: Bank statements Purchase & sales invoices Expense bills and vouchers GST returns (GSTR-1, GSTR-3B) Income tax returns Statutory Records: Register of members Board meeting minutes Shareholding records Why Audit is Important for a Private Limited Company Audit plays a vital role in maintaining the financial discipline and legal compliance of a Private Limited Company. It helps businesses comply with the provisions of the Companies Act, 2013, Income Tax Act, and other regulatory laws while ensuring timely ROC and tax filings. Audited financial statements improve the company’s credibility among investors, banks, shareholders, and financial institutions by proving that financial records are accurate and trustworthy. Audits also enhance transparency by presenting a true picture of the company’s financial position. They help identify weaknesses in internal controls, accounting systems, and operational procedures, leading to better management and efficiency. Regular audits further assist in detecting accounting errors, fraud, and financial irregularities at an early stage, reducing the possibility of major losses. In addition, audits help companies avoid penalties, legal disputes, and non-compliance issues. Since audited financial statements are often required for loans, investments, tenders, and business expansion, audits also support long-term business growth and strengthen stakeholder confidence. Audit compliance is not just a statutory requirement it is a foundation of financial integrity and business success. Every private limited company must treat audits as a strategic function, not just a yearly obligation. By maintaining proper records, appointing auditors on time, and ensuring timely filing’s, businesses can avoid penalties and build a strong, credible financial reputation.

Companies incorporated between January and March can hold their first AGM within 9 months from the end of the financial year.

Filed for appointment or reappointment of the auditor within 15 days of the AGM or Board resolution.

Used for filing audited financial statements, Board’s Report, and Auditor’s Report within 30 days of the AGM.

Filed for submission of the company’s annual return within 60 days of the AGM.

Applicable for filing the tax audit report under Section 44AB of the Income Tax Act, where tax audit provisions apply.Documents Required for Company Audit

Conclusion

© 2026 Tax Esquire | Expert CA Services in Greater Noida, Uttar Pradesh

8810380146 | info.taxesquire@gmail.com | taxesquire.in

This document is for informational purposes only. For personalised tax advice, consult our chartered accountants.