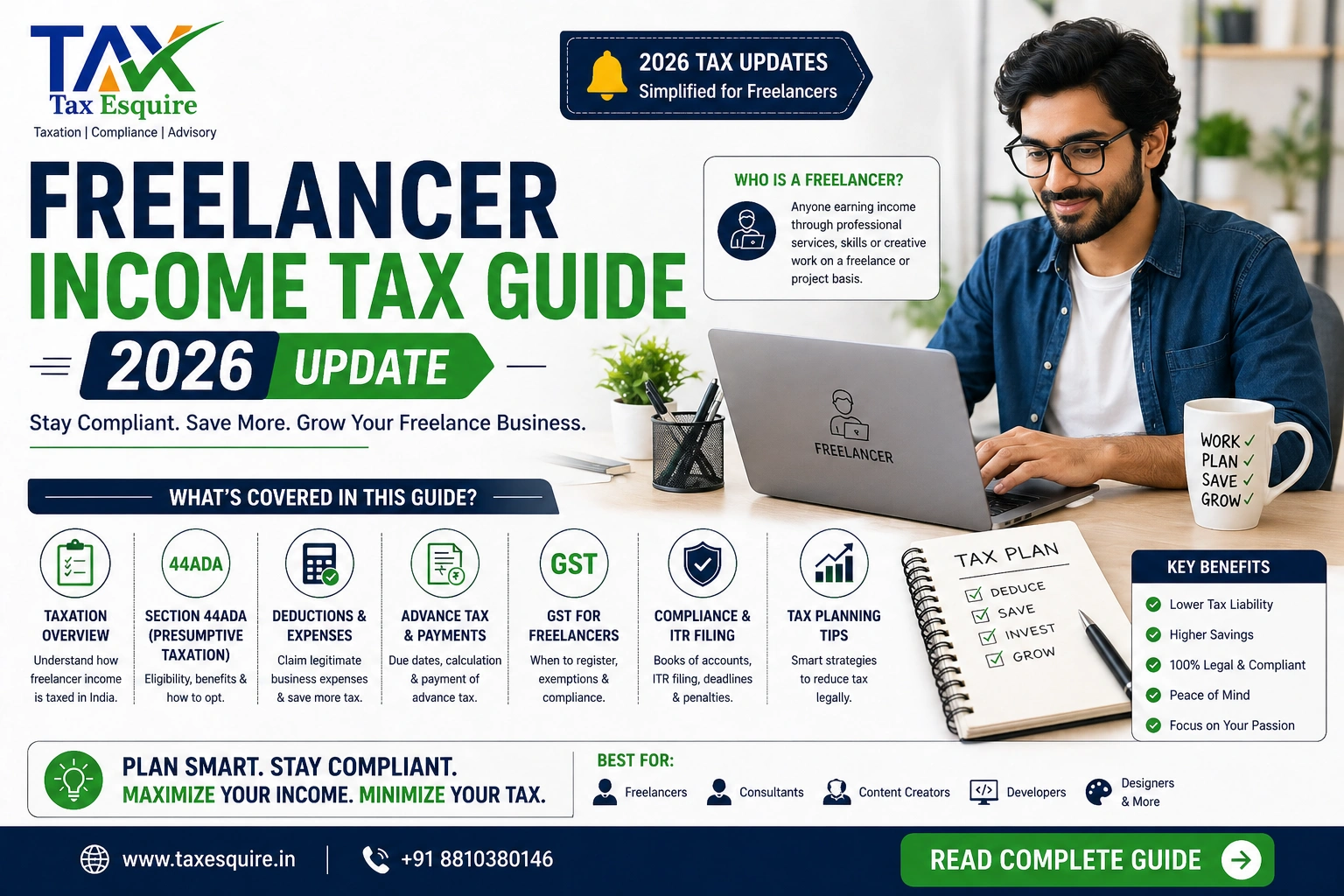

Freelancer Income Tax Guide : 2026 Update

Introduction

Freelancing in India has grown rapidly with the rise of the digital economy, remote work, and global clients. From designers and developers to influencers and consultants, more professionals are choosing independent work over traditional employment.

However, with flexibility comes tax responsibility. Unlike salaried individuals, freelancers must handle their own:

Income reporting

Tax payments

Compliance (GST, TDS, advance tax)

For FY 2025–26 (AY 2026–27), understanding updated tax rules is crucial to :

Avoid penalties

Reduce tax liability

Maintain financial discipline

This guide covers everything—from basics to advanced tax strategies.

Who is a freelancer as per income tax?

Under the Income Tax Act, a freelancer is generally treated as a professional or self-employed individual earning income through independent services.

Examples:

Graphic designers, developers, writers

Chartered accountants, lawyers, consultants

YouTubers, influencers, bloggers

Digital marketers, coaches

Income is taxed under the following:

“Profits & Gains from Business or Profession (PGBP)”

Types of Taxes Applicable to Freelancers

Freelancer’s may be subject to multiple taxes:

Income Tax: Based on total annual income

GST (Goods & Services Tax): Applicable if turnover exceed’s threshold or for interstate/export services

TDS (Tax Deducted at Source): Deducted by clients before payment

Advance Tax: Paid quarterly if tax liability exceeds ₹10,000

Income Tax on Freelancers

Freelancers calculate income as:

Total Income = Gross Receipts – Expenses

Key Points:

All earning’s must be reported (including foreign income)

Maintain invoices and payment proof’s

Convert foreign income into INR as per RBI rates

Old vs New Tax Regime (2026 Comparison)

Freelancers can choose between two tax regimes:

Old Regime: Allows deductions (80C, 80D, expenses) and Higher tax rates

New Regime

Lower tax rates

Limited deductions

Which is better?

Choose Old Regime → if you have high deductions

Choose New Regime → if you prefer simplicity

Presumptive Taxation Scheme (Section 44ADA)

A major benefit for freelancers.

Eligibility: Professionals with income up to ₹75 lakh (subject to conditions)

Tax Rule: 50% of income considered profit and No need to maintain detailed books

Benefits:

Simple compliance

No audit required

Saves time

Normal Taxation (If Not Opting 44ADA)

If you don’t opt for presumptive taxation:

Requirements:

Maintain books of accounts

Track all income & expenses

Audit required if limits exceed

Important: Accurate bookkeeping helps reduce tax through legitimate expenses.

Deductions Available for Freelancers

Freelancers can claim various deductions:

Business Expenses:

Internet, electricity

Laptop, software tools

Office rent

Travel expenses

Depreciation:

On assets like laptops, furniture

Personal Deductions:

Section 80C (PPF, ELSS, LIC)

Section 80D (Health Insurance)

NPS (80CCD)

Smart deductions = lower tax liability

GST for Freelancers

When GST is required:

Turnover exceeds ₹20 lakh (₹10 lakh for special states)

Interstate services

Export of services

Key Concepts:

GST rate usually 18%

Export services → zero-rated (LUT benefit)

Compliance:

GST registration

Monthly/quarterly returns

TDS on Freelance Income

Applicable Sections:

194J (Professional services)

194C (Contracts)

TDS Rate:

Usually 10% under 194J

Important:

Check Form 26AS / AIS

Claim TDS credit while filing ITR

Advance Tax for Freelancers

If tax liability exceeds ₹10,000:

Due Dates:

15 June – 15%

15 Sept – 45%

15 Dec – 75%

15 March – 100%

Penalty: Interest under Sections 234B & 234C

Filing ITR for Freelancers

Applicable Forms:

ITR-3 → Normal taxation

ITR-4 → Presumptive (44ADA)

Process:

Calculate income

Claim deductions

Verify TDS

File and e-verify

Common mistakes:

Wrong ITR form

Missing income

Ignoring GST mismatch

Read the rest in 'Freelancer Income Tax Guide : 2026 Update Part - 2 - Click Here