Common Mistakes in ITR Filing 2026 That Can Trigger Notice

Introduction

Filing an Income Tax Return (ITR) is a statutory obligation for taxpayers, but in 2026, it has evolved into a highly monitored and data-driven compliance process. The Income Tax Department now relies heavily on automated systems, real-time reporting, and financial data integration to verify the accuracy of every return filed.

As a result, even minor discrepancies whether intentional or accidental can lead to tax notices, penalties, delayed refunds, or scrutiny assessments. Many taxpayers assume that small errors will go unnoticed, but with systems like AIS (Annual Information Statement) and TIS (Taxpayer Information Summary), almost every financial transaction is tracked.

This blog provides a comprehensive guide to the most common ITR filing mistakes in 2026, explains why they trigger notices, and outlines practical steps to avoid them.

Why Income Tax Notices Are Increasing in 2026

The significant increase in income tax notices in recent years is primarily due to technological advancements and stricter compliance enforcement.

The Income Tax Department has adopted Artificial Intelligence (AI) and data analytics tools to identify inconsistencies between taxpayer filings and third-party data. Financial institutions such as banks, stock brokers, employers, and registrars report transaction details directly to the department..

Key reasons for increased notices include:

AIS & TIS Integration: These systems consolidate all financial transactions, including interest income, stock trades, and high-value purchases.

Pre-filled ITR Forms: The department already has your financial data—any deviation raises a red flag.

Real-Time Data Matching: Automated systems compare filed returns with Form 26AS, AIS, and other records instantly.

Stronger Compliance Measures: The government aims to reduce tax evasion and improve transparency.

As a result, the margin for error has reduced significantly, making accurate filing more critical than ever.

Types of Income Tax Notices

Understanding different types of notices helps taxpayers respond effectively and avoid escalation.

Section 139(9) - Defective Return: Issued when the return contains errors or incomplete information. If not corrected within the specified time, the return may be treated as invalid.

Section 143(1) – Intimation Notice: A preliminary assessment where the department highlights mismatches in income, deductions, or tax calculations.

Section 143(2) – Scrutiny Notice: Issued when the department wants a detailed review of your return. This may involve submitting additional documents and explanations.

Section 148 – Income Escaping Assessment: Issued when the department believes income has not been disclosed or has been underreported.

Each notice has legal implications, and timely action is essential to avoid penalties.

Top Common Mistakes in ITR Filing (2026)

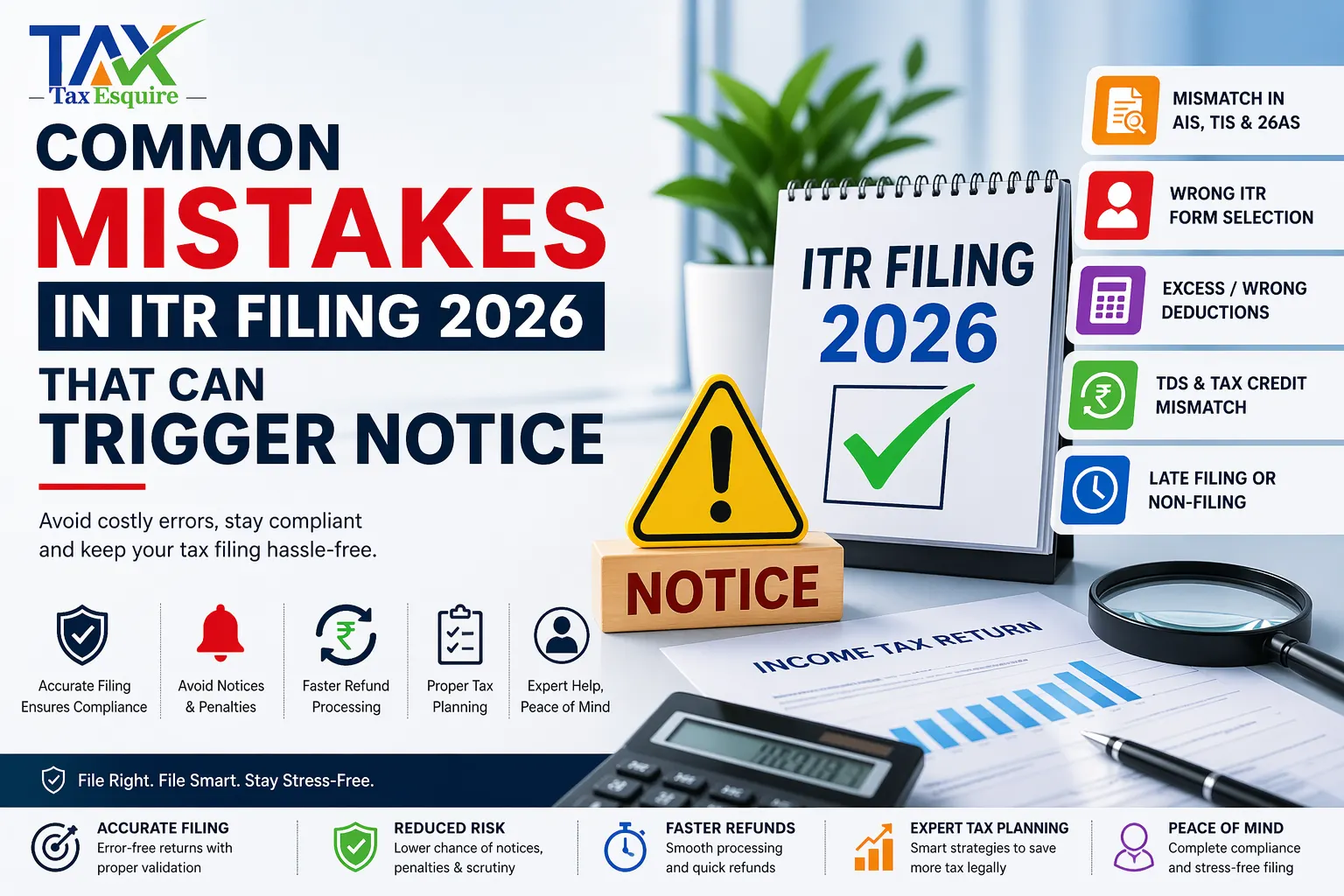

1. Mismatch with AIS, TIS & Form 26AS

One of the most common mistakes is failing to reconcile your return with official records. AIS and TIS capture detailed financial data, while Form 26AS reflects tax credits.

If the income reported in your ITR does not match these records, it may trigger an automated notice. This often happens when taxpayers ignore small income entries like interest or dividend income.

2. Incorrect Personal & Bank Details

Errors in personal information can lead to processing failures and compliance issues.

Incorrect PAN, Aadhaar mismatch, or wrong bank account details may result in:

Rejected returns

Failed refund transfers

Additional verification requirements

Accuracy in these details is essential for smooth processing.

3. Not Reporting All Sources of Income

Many taxpayers mistakenly believe that only primary income (salary/business) needs to be reported. However, all sources must be disclosed, including:

Interest from savings accounts and fixed deposits

Freelance or side income

Rental income

Capital gains from investments

Non-reporting of income is easily detected through AIS and can directly trigger notices.

4. Wrong ITR Form Selection

Selecting the correct ITR form is crucial. Each form is designed for specific income categories.

For example, filing ITR-1 when you have capital gains or business income can result in your return being considered defective. This mistake may require refiling and can delay processing.

5. Claiming Excess or Wrong Deductions

Overstating deductions or claiming ineligible exemptions is a serious compliance issue.

Common errors include:

Claiming deductions without proof

Double claiming the same benefit

Applying deductions not allowed under the chosen tax regime

Such discrepancies are easily flagged and may lead to scrutiny.

6. Mismatch in TDS & Tax Credit

Tax Deducted at Source (TDS) must match the records in Form 26AS.If you claim excess TDS or fail to report TDS correctly, the department may issue an intimation notice. This often occurs due to incorrect data entry or missing updates from deductors.

7. Late Filing or Non-Filing of Return

Missing deadlines not only attracts penalties but also increases the chances of scrutiny.

Late filing may lead to:

Interest on unpaid tax

Loss of carry-forward benefits

Increased monitoring by tax authorities

Consistent non-filing can result in legal consequences.

8. Incorrect Reporting of Capital Gains

Capital gains transactions are closely monitored due to their complexity and high tax impact.

Errors may include:

Incorrect calculation of gains

Ignoring indexation benefits

Not reporting stock or crypto transactions

Such mistakes often trigger scrutiny notices.

9. Not Verifying the ITR

Many taxpayers forget that filing is incomplete without verification.If the ITR is not e-verified within the specified time, it is treated as invalid, meaning it is considered as not filed at all. This can lead to penalties and compliance issues.

10. Ignoring Notices or Emails from IT Department

Ignoring communication from the Income Tax Department is a critical mistake.

Failure to respond within deadlines can result in:

Penalties

Escalation to scrutiny

Legal action in severe cases

Prompt action is always advisable.

High-Risk Transactions That Trigger Tax Notices

Certain financial activities are automatically tracked and flagged for review:

Large cash deposits in bank accounts

High-value property transactions

Significant credit card expenditures

Foreign investments or remittances

If these transactions are not properly reported or justified, they may trigger notices.

Consequences of Filing Incorrect ITR

Incorrect filing can have serious consequences beyond simple corrections. These include:

Financial penalties and interest on unpaid taxes

Delay or rejection of refunds

Scrutiny assessments requiring detailed explanations

Legal proceedings in cases of significant discrepancies

Ensuring accuracy is essential to avoid these risks.

How to Avoid ITR Filing Mistakes in 2026

Preventing mistakes requires a systematic approach:

Carefully reconcile AIS, TIS, and Form 26AS

Maintain proper documentation for income and deductions

Choose the correct ITR form based on income sources

Report all income, even if it seems minor

File returns before the due date

Complete e-verification promptly

Taking these steps significantly reduces the risk of notices.

What to Do If You Receive a Tax Notice

Receiving a notice is not uncommon and should not cause panic.

Steps to follow:

Carefully read and understand the notice

Identify the issue or discrepancy

Gather supporting documents

Respond within the given deadline

Seek professional assistance if required

Timely and accurate responses can resolve most issues without escalation.

Benefits of Filing Accurate ITR with Expert Help

Filing an Income Tax Return (ITR) may appear straightforward, especially with pre-filled data and online utilities. However, the increasing complexity of tax laws, frequent regulatory updates, and deep data verification systems make professional assistance more valuable than ever in 2026.

Engaging a qualified tax expert—such as a Chartered Accountant or tax consultant—ensures that your return is not only filed correctly but also strategically optimized for compliance and efficiency. Below are the key benefits explained in detail:

Error-Free Filing with Proper Validation: One of the biggest advantages of expert assistance is accuracy. Tax professionals follow a structured process to validate every detail before submission.

They ensure:

Proper reconciliation of AIS, TIS, and Form 26AS

Correct classification of income (salary, business, capital gains, etc.)

Accurate calculation of tax liability

Valid claim of deductions and exemptions

Even small errors—such as incorrect figures or missing entries—can trigger notices. Experts minimize these risks through multi-level verification and compliance checks.

Reduced Risk of Notices and Penalties: Income tax notices are often triggered by mismatches, omissions, or incorrect claims. Professionals are well-versed in identifying high-risk areas and ensuring compliance with current tax regulations.

They help:

Avoid discrepancies in reported income

Ensure proper disclosure of all financial transactions

Prevent incorrect deduction claims

Align return data with government records

This significantly lowers the chances of receiving notices under sections like 143(1), 139(9), or scrutiny cases, ultimately protecting you from penalties and legal complications.

Faster Refund Processing: A correctly filed and verified ITR is processed much faster by the Income Tax Department. Errors or mismatches often lead to refund delays or rejections.

Tax experts ensure:

Accurate bank details for refund credit

Proper tax credit claims

Complete and timely e-verification

Compliance with all processing requirements

As a result, refunds are issued smoothly and without unnecessary delays, improving your overall experience.

Expert Guidance on Tax Planning: Beyond filing returns, professionals provide valuable insights into tax planning and optimization.

They help you:

Choose between old vs new tax regime

Maximize eligible deductions and exemptions

Plan investments for tax savings

Structure income efficiently to reduce tax liability

This proactive approach ensures that you not only remain compliant but also legally minimize your tax burden.

Peace of Mind and Compliance Assurance: Tax compliance can be stressful, especially with evolving laws and strict scrutiny systems. With expert assistance, you gain confidence and peace of mind knowing that your return is handled professionally. You don’t have to worry about: Missing deadlines Incorrect filings Responding to complex notices Keeping up with changing tax rules Professionals ensure that your tax matters are fully compliant, up-to-date, and risk-free, allowing you to focus on your business or personal priorities. Expert help becomes even more critical in cases involving: Multiple income sources Business or professional income Capital gains from shares, property, or crypto Foreign income or assets High-value transactions Such scenarios require technical expertise, proper documentation, and strategic reporting, which only experienced professionals can handle effectively. In 2026, the Income Tax system is more transparent, automated, and strict than ever before. Most tax notices are not random—they are triggered by avoidable mistakes such as mismatched data, incorrect deductions, or unreported income.By understanding these common errors and following best practices, taxpayers can ensure accurate filing, avoid notices, and maintain smooth compliance. Taking a proactive approach—or seeking expert assistance—can save time, money, and unnecessary stress.Essential for Complex Tax Situations

Conclusion

© 2026 Tax Esquire | Expert CA Services in Greater Noida, Uttar Pradesh

8810380146 | info.taxesquire@gmail.com | taxesquire.in

This document is for informational purposes only. For personalised tax advice, consult our chartered accountants.