Income Tax Act 1961 vs 2025: Major Changes Explained

In Indian taxation system has undergone significant transformation since the introduction of the Income Tax Act, 1961. Over the decade’s, amendments have been made to align taxation with economic growth, compliance need’s, and global standard’s. However, the change’s introduced around 2025 mark a notable shift toward simplification, digitalization, and taxpayer convenience.

This blog explore’s the key difference’s between the original framework of the Income Tax Act, 1961 and the major change’s introduced by 2025.

1. Structural Evolution of the Tax System

Income Tax Act, 1961

The original Act was comprehensive but complex, with numerou’s section’s, proviso’s, and frequent amendment’s. Taxpayer’s often required professional assistance to interpret provision’s.

2025 Changes

By 2025, the tax structure has been simplified significantly:

● Introduction of streamlined tax regimes

● Reduction in complex exemptions and deductions

● Greater clarity in provisions

2. Old Tax Regime vs New Tax Regime

1961 Framework

The traditional tax system allowed multiple deductions such as:

● Section 80C

● House Rent Allowance (HRA)

● Standard deductions

2025 Scenario

The new tax regime has become the default system:

● Lower tax rates

● Minimal or no deductions

● Optional shift to old regime still available (with conditions)

3. What Exactly Changed?

Here’s a direct comparison of the most important changes:

|

Area |

1961 System |

2025 System |

|

Tax Approach |

Deduction-based |

Low-rate simplified system |

|

Tax Regime |

Only one regime |

New regime is default |

|

Filing |

Manual / paper-based |

Fully online & pre-filled |

|

Income Tracking |

Limited |

AIS & full data tracking |

|

Refunds |

Slow (months) |

Fast (days/weeks) |

|

Compliance |

Moderate |

Strict with AI monitoring |

|

Identity |

Separate PAN |

PAN-Aadhaar linked |

|

|

|

|

4. Digitalization of Tax Administration

1961 Era

● Manual filing of returns

● Physical documentation

● High dependency on tax officers

2025 Advancements

● Fully online filing systems

● Pre-filled Income Tax Returns (ITRs)

● AI-based scrutiny and processing

● Faceless assessment and appeals

5. Compliance and Reporting Requirements

Earlier System

Compliance was documentation-heavy and time consuming. Tracking income source’s and reporting was largely manual.

2025 Updates

● Integration with PAN, Aadhaar, and financial institution’s

● Automatic reporting of income (salary, interest, capital gains)

● Real time data sharing between agencie’s

6. Focus on Transparency and Anti-Evasion

1961 Approach

Tax evasion was a major concern due to limited tracking mechanism’s.

2025 Reforms

● Use of data analytics and AI

● Stricter penaltie’s for undisclosed income

● Global information exchange agreement’s

7. Changes in Capital Gains Taxation

Earlier Provisions

Capital gains taxation varied significantly based on asset type and holding period, often leading to confusion.

2025 Developments

● Rationalization of holding periods

● Simplified tax rates

● Improved reporting mechanisms

8. Corporate Tax Reforms

1961 Structure

Higher corporate tax rates with multiple exemptions.

2025 Scenario

● Reduced corporate tax rates

● Incentives for new manufacturing companies

● Removal of unnecessary exemptions

9. Ease of Doing Taxes

Then (1961)

Taxation was perceived as complicated and time-consuming.

Now (2025)

● User-friendly tax portal’s

● Faster refund’s

● Simplified grievance redressal

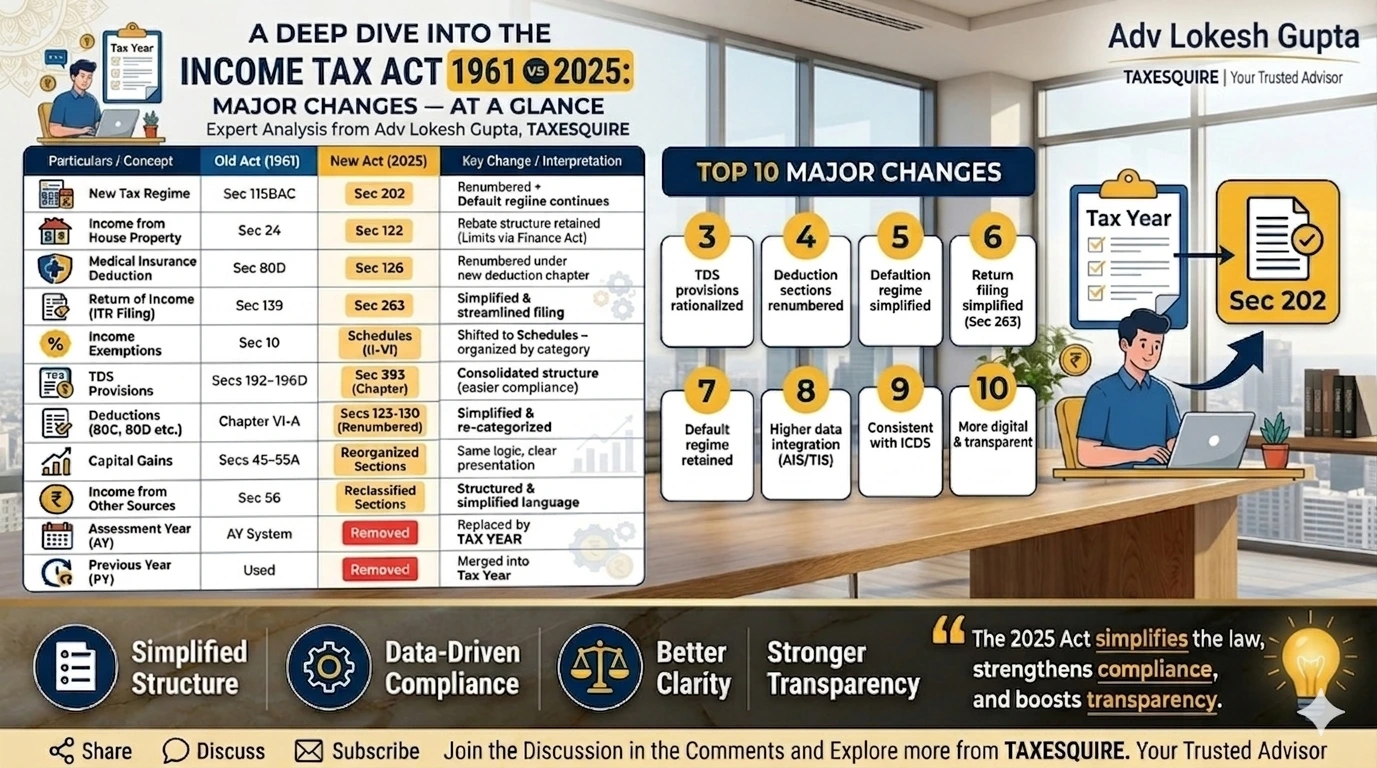

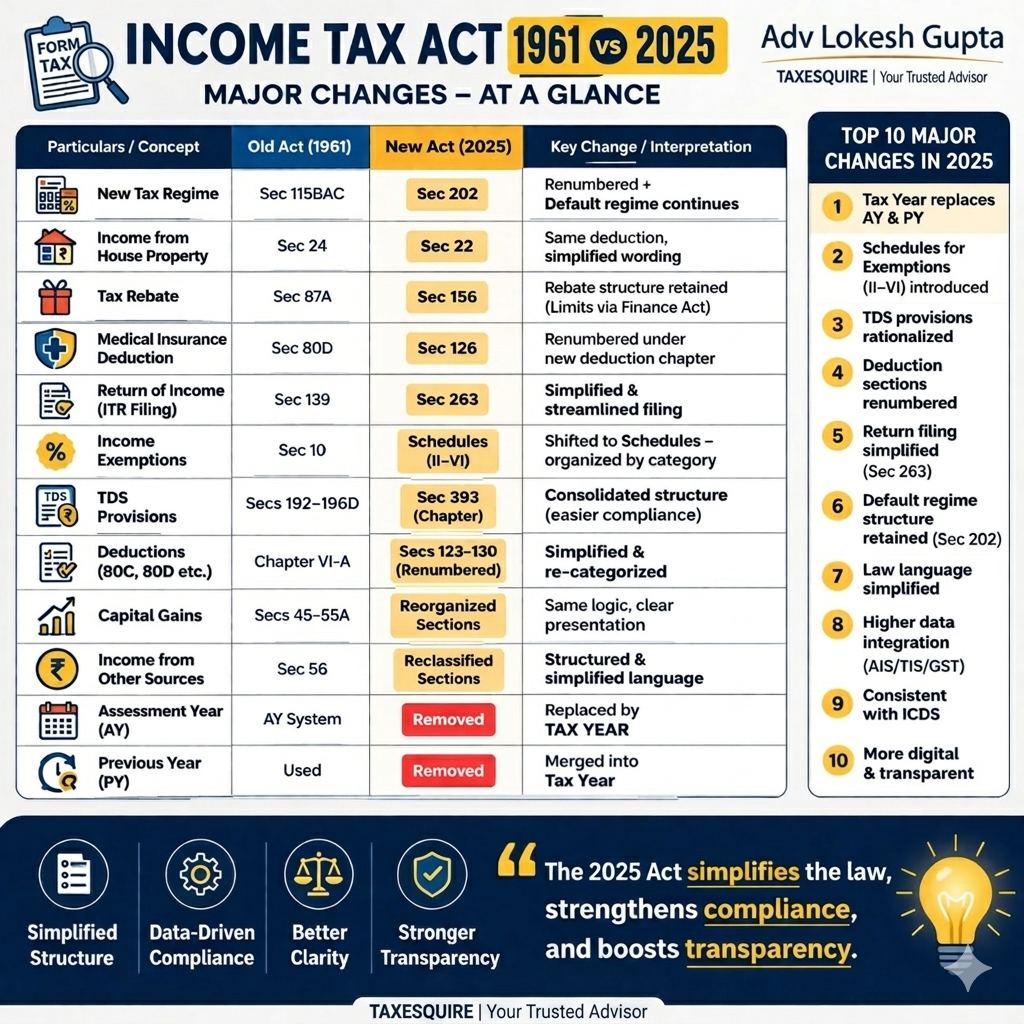

Deductions Under the Income Tax Act 2025

Despite potential changes to section numbering and organization, the new law maintains many deductions.

|

Deduction |

Income Tax Act 1961 |

Income Tax Act 2025 |

|

Salary income definition |

Sec 15 |

Sec 15 |

|

Standard deduction (salary) |

Sec 16(ia) |

Sec 19 |

|

Professional tax deduction |

Sec 16(iii) |

Sec 19 |

|

Perquisites |

Sec 17 |

Sec 17 |

|

Income from house property |

Sec 22 |

Sec 20 |

|

Annual value of house property |

Sec 23 |

Sec 21 |

|

Home loan interest |

Sec 24(b) |

Sec 22 |

|

80C investments |

Sec 80C |

Sec 123 |

|

Pension or annuity |

Sec 80CCC |

Sec 123 |

|

NPS deduction |

Sec 80CCD |

Sec 124 |

|

Health insurance |

Sec 80D |

Sec 126 |

|

Education loan interest |

Sec 80E |

Sec 129 |

|

Donations |

Sec 80G |

Sec 133 |

|

Savings account interest |

Sec 80TTA |

Sec 153 |

|

Rebate |

Sec 87A |

Sec 156 |

|

HRA exemption |

Sec 10(13A) |

Schedule for income not forming part of total income |

|

Leave Travel Allowance |

Sec 10(5) |

Schedule for exempt allowances |

|

Gratuity exemption |

Sec 10(10) |

Schedule for exempt retirement benefits |

|

Leave encashment |

Sec 10(10AA) |

Same schedule under exempt income |

© 2026 Tax Esquire | Expert CA Services in Greater Noida, Uttar Pradesh

8810380146 | info.taxesquire@gmail.com | taxesquire.in

This document is for informational purposes only. For personalised tax advice, consult our chartered accountants.