What is Concept of Tax Year in the New Income Tax Act, 2025

Introduction

India’s taxation framework is set for a major transformation with the proposed Income Tax Act, 2025. One of the most significant reforms is the introduction of the Tax Year, replacing the long-standing and often confusing concepts of Financial Year (FY) and Assessment Year (AY).

For decades, taxpayers in India have followed a dual-year system where income is earned in one year and taxed in another. While administratively functional, this structure has frequently led to confusion, especially among individuals, small businesses, and new taxpayers.

The new system aims to simplify this approach by introducing a single, unified timeline making tax compliance more intuitive, transparent, and aligned with global practices.

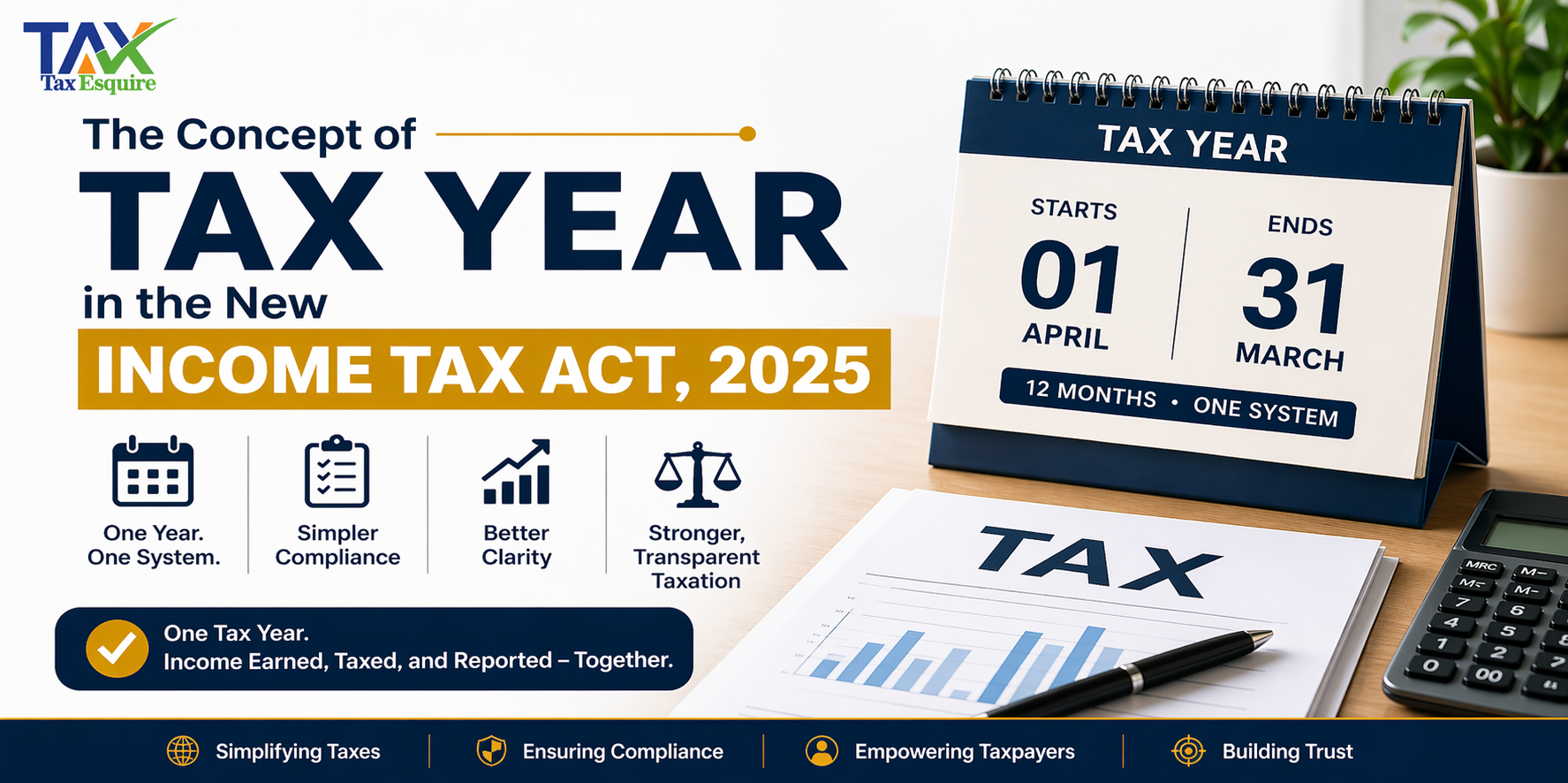

What is a Tax Year?

Under the proposed law, a Tax Year refers to a 12-month period during which income is earned and taxed within the same timeframe.

Key Features of Tax Year:

Begins on 1st April

Ends on 31st March

Covers income earning, reporting, and taxation together

In simple terms: Income earned during a year is taxed for that same year—no separate assessment period.

This eliminates the need to differentiate between when income is earned and when it is assessed, making the system far easier to understand and follow.

Financial Year vs Assessment Year vs Tax Year

To fully appreciate this reform, it is important to understand how the earlier system worked and how the new model improves it.

Old System: Financial Year (FY) & Assessment Year (AY)

Financial Year (FY) – Income Period

The Financial Year is the period in which income is earned.

Example: Income earned from 1 April 2024 to 31 March 2025 falls under FY 2024–25.

Assessment Year (AY) – Taxation Period

The Assessment Year is the following year in which:

Income is reported

Taxes are calculated

Returns are filed

Example: Income of FY 2024–25 is assessed in AY 2025–26.

Problem with the Old System

Two different terms for one income cycle

Frequent confusion while filing returns

Difficulty in understanding timelines

New System: Tax Year

The new law replaces this dual structure with a single concept — the Tax Year.

No separate Assessment Year

Income and taxation belong to the same period

Simplified compliance and reporting

Key Differences at a Glance

This shift removes the one-year gap and simplifies the entire taxation process.

Why Was the Tax Year Introduced?

The introduction of the Tax Year is not just a cosmetic change—it is a structural reform aimed at improving the tax ecosystem.

Key Reasons:

Simplification: Eliminates confusion between FY and AY

Ease of Compliance: Makes return filing more straightforward

Global Alignment: Matches international tax systems

Administrative Efficiency: Reduces duplication in records and communication

Overall, the goal is to make taxation more user-friendly and transparent.

Applicability of Tax Year (Who Will It Affect?)

The Tax Year framework applies broadly across all categories of taxpayers:

Individuals: Salaried employees and freelancers will find tax filing easier due to simplified timelines.

Businesses & Corporates: Companies will need to align accounting systems and compliance processes with the new structure.

Professionals & Startups: Consultants and startups benefit from reduced ambiguity and better clarity in reporting.

Non-Residents: Non-resident taxpayers will also follow the Tax Year, subject to specific provisions.

How the Tax Year Works in Practice

The functioning of the Tax Year is straightforward:

Income is earned between April 1 and March 31

Tax liability is calculated for the same period

Returns are filed for that same Tax Year

No need to track a separate “assessment year,” reducing errors and confusion.

Transition from Old System to New Tax Year

Moving from the FY–AY model to the Tax Year system requires a structured transition.

Key Transition Points:

Existing assessments under the old system will continue until completion

New filings will adopt the Tax Year concept

Transitional provisions may be introduced to avoid overlap

Taxpayers and professionals must stay updated with official notifications during this phase.

Impact on Taxpayers

Positive Impact

Clear and simple tax timelines

Reduced filing errors

Better understanding of tax obligations

Adjustment Areas

Learning new terminology

Updating financial habits and documentation

Overall, the reform is particularly beneficial for small and mid-level taxpayers.

Impact on Businesses & Professionals

Operational Impact

Updates in accounting and ERP systems

Changes in compliance documentation

Strategic Impact

Revised tax planning strategies

Alignment of audit and reporting cycles

Professional advisors will play a critical role in ensuring smooth adaptation.

Key Benefits of the Tax Year System

The Tax Year system offers several long-term advantages:

Clarity: Single timeline replaces dual concepts

Consistency: Uniform understanding across taxpayers

Efficiency: Streamlined compliance process

Global Compatibility: Aligns with international standards

This reform enhances the overall taxpayer experience.

Challenges & Criticism of the New System

Despite its advantages, certain challenges may arise:

Initial confusion during implementation

Need for software and system upgrade’s

Training requirements for professionals

Short-term compliance disruptions

The effectiveness of this reform will depend largely on smooth execution and awareness.

Expert Insights & Recommendations

Tax professionals suggest the following:

Stay updated with government notifications

Upgrade accounting and compliance systems

Educate teams and clients about the new concept

Plan taxes proactively under the new framework

Early preparation will ensure a smooth transition.

Conclusion

The introduction of the Tax Year under the Income Tax Act, 2025 marks a significant evolution in India’s tax system. By eliminating the long-standing distinction between Financial Year and Assessment Year, the government aims to simplify compliance and improve clarity for taxpayers.

While the transition phase may require some adjustment, the long-term benefits such as improved transparency, reduced complexity, and enhanced efficiency make this reform a forward-looking step in India’s tax landscape.

Author: CA POONAM GUPTA & ADV LOKESH GUPTA

© 2026 Tax Esquire | Expert CA Services in Greater Noida, Uttar Pradesh

8810380146 | info.taxesquire@gmail.com | taxesquire.in

This document is for informational purposes only. For personalised tax advice, consult our chartered accountants.