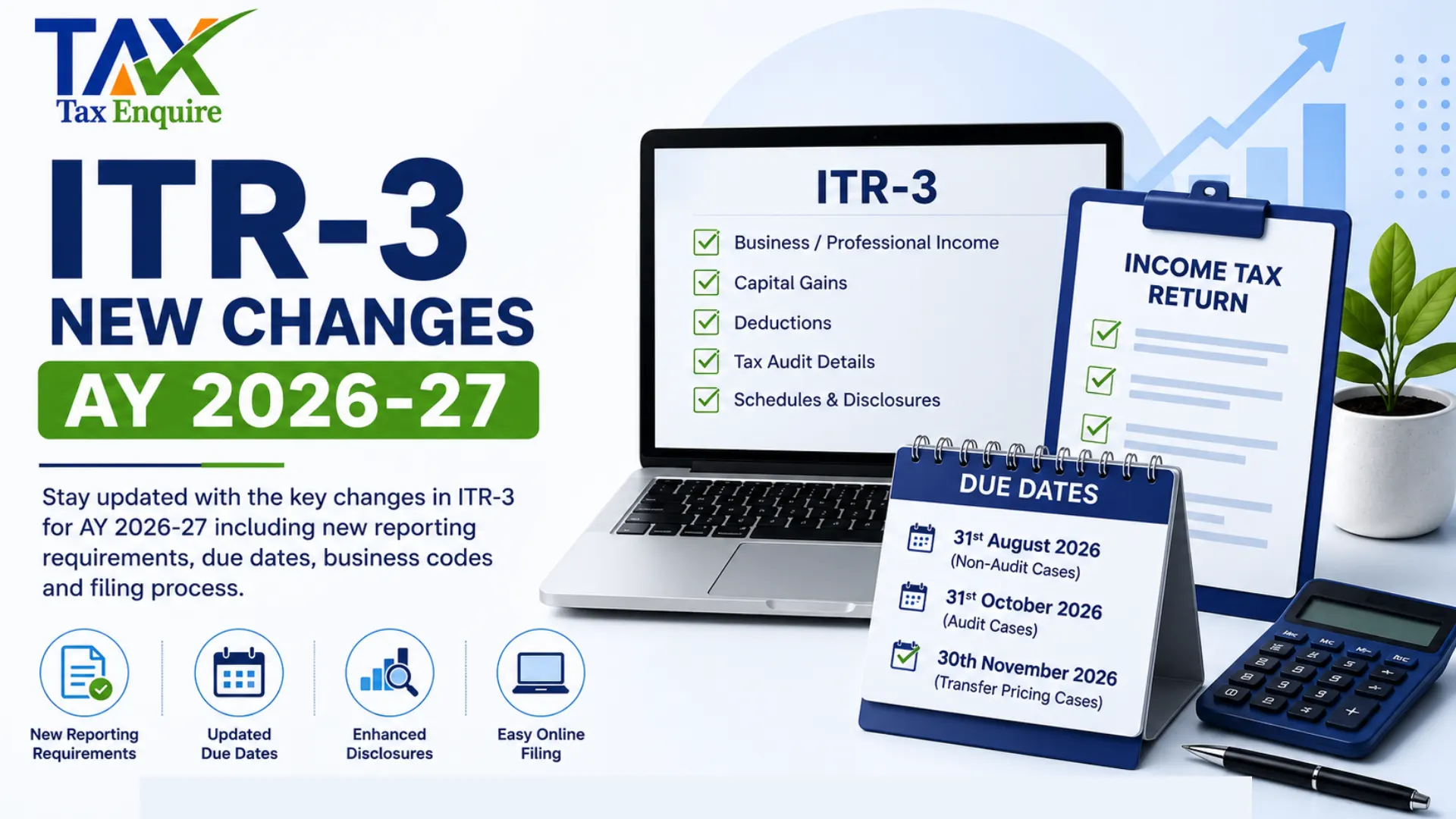

ITR-4 New Changes AY 2026-27

Introduction

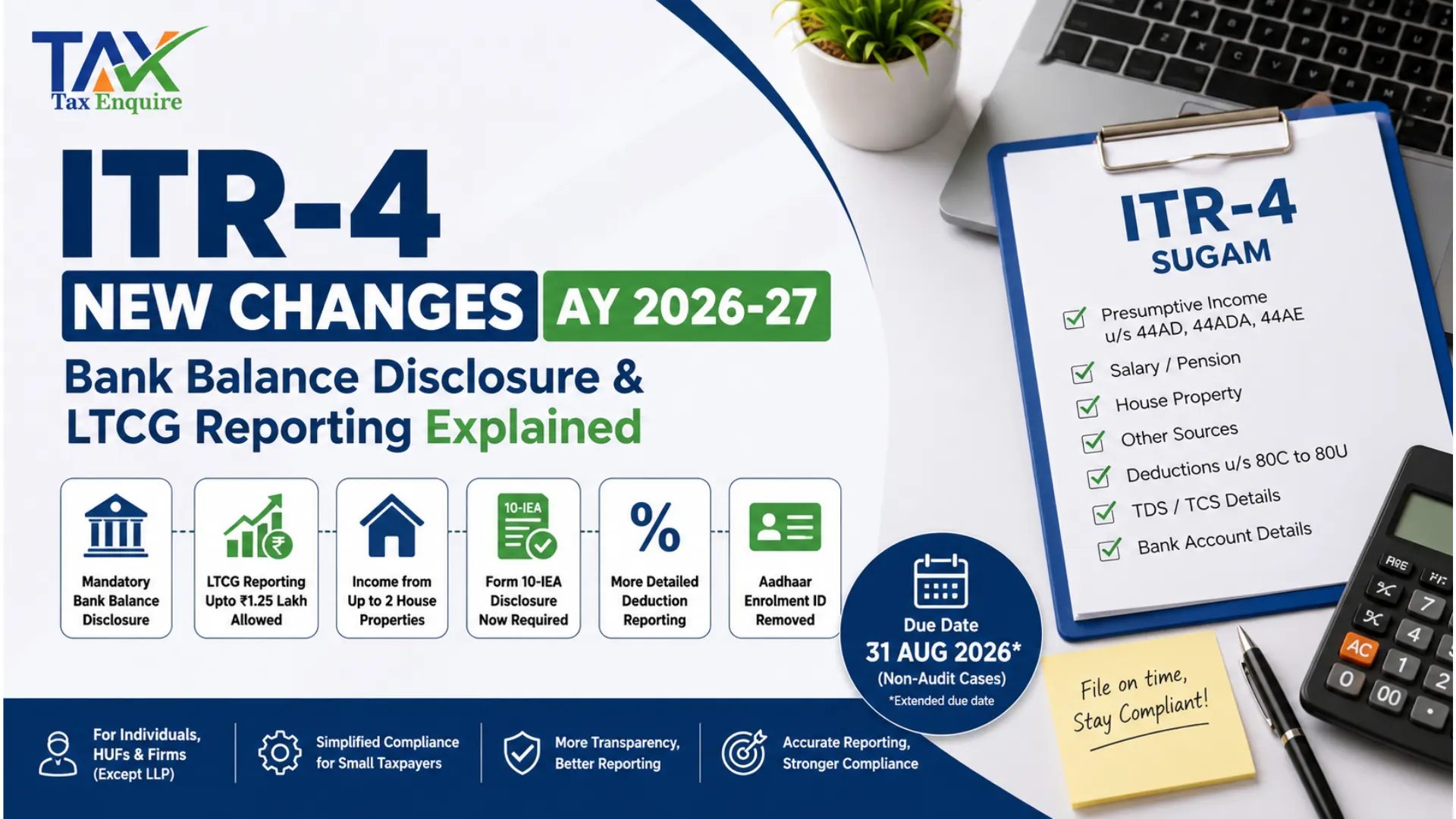

Filing Income Tax Return (ITR) has become more detailed for small taxpayers and professionals in Assessment Year (AY) 2026-27. The Central Board of Direct Taxes (CBDT) has introduced several important changes in the ITR-4 (Sugam) form to improve transparency and simplify compliance for taxpayers opting for presumptive taxation schemes under Sections 44AD, 44ADA, and 44AE.

One of the major updates is the mandatory disclosure of bank balances in the ITR-4 form. In addition, taxpayers can now report Long-Term Capital Gains (LTCG) under Section 112A within specified limits directly in ITR-4. These changes are aimed at making tax reporting more accurate and reducing the need for taxpayers to shift to complex ITR forms.

In this article, we will understand who can file ITR-4, who cannot file it, the due date for filing, structure of the form, online filing process, and the latest changes applicable from AY 2026-27.

Who Qualifies for Filing ITR-4?

ITR-4 (Sugam) can be filed by Resident Individuals, Hindu Undivided Families (HUFs), and Partnership Firms (excluding LLPs) who opt for presumptive taxation schemes and have total income up to ₹50 lakh during the financial year.

A taxpayer can file ITR-4 if they have:

Business income under Section 44AD

Professional income under Section 44ADA

Income from goods carriage business under Section 44AE

Salary or pension income

Income from one or two house properties

Income from other sources such as interest

Long-Term Capital Gains (LTCG) under Section 112A up to ₹1.25 lakh without carried forward losses

ITR-4 is mainly designed for small taxpayers who prefer simplified tax compliance and do not maintain detailed books of accounts.

Taxpayers Not Eligible for ITR-4 A taxpayer cannot use ITR-4 in the following situations: Total income exceeds ₹50 lakh The taxpayer is a Non-Resident (NRI) or Resident Not Ordinarily Resident (RNOR) The taxpayer owns foreign assets or has foreign income Income arises from more than two house properties Capital gains exceed the prescribed LTCG limit Carry forward or set-off of capital losses is required Income is earned from lottery, horse racing, or speculative business The taxpayer is a Director in a company Investment in unlisted equity shares exists The taxpayer is an LLP Agricultural income exceeds ₹5,000 Taxpayers not eligible for ITR-4 generally need to file ITR-2 or ITR-3 depending on the nature of income. Due Date to File ITR-4 For FY 2025-26 (AY 2026-27) The due date for filing ITR-4 depends on whether the taxpayer is required to get accounts audited. Budget 2026 extended the due date for non-audit taxpayers from 31 July to 31 August 2026, giving small taxpayers additional time to complete compliance requirements. Taxpayers should file returns before the due date to avoid penalties, interest, and loss of certain tax benefits. What is the Structure of ITR-4? The ITR-4 form is divided into different parts and schedules to capture complete financial details of the taxpayer. Main Parts of ITR-4 PART A: General Information PART B: Gross total income from the five heads of income PART C: Deduction and total taxable income PART D: Tax computation and tax status Information regarding turnover/Gross receipts reported for GST: Furnish the GSTIN Schedule BP: Schedule TDS/TCS: Financial Particulars: Bank Account Details: How to File ITR-4 Online on Income Tax Portal? Taxpayers can easily file ITR-4 online through the Income Tax e-Filing portal by following these steps: Step 1: Visit the Income Tax Portal Go to the official Income Tax e-Filing portal. Step 2: Login to Your Account Enter: PAN/User ID Password Captcha code Step 3: Select “File Income Tax Return” Choose: Assessment Year: AY 2026-27 Online filing mode Status as Individual/HUF/Firm Step 4: Choose ITR-4 Form Select ITR-4 (Sugam) from the list of available ITR forms. Step 5: Enter Income & Deduction Details Fill details related to: Presumptive income Salary House property Interest income Deductions Step 6: Provide Bank Account Information Enter all active bank accounts and disclose closing bank balance as on 31 March 2026. Step 7: Verify Tax Details Cross-check: AIS Form 26AS TDS details Advance tax Step 8: Preview & Submit Return Review all information carefully and submit the return. Step 9: Verify the Return Complete verification through: Aadhaar OTP Net banking DSC EVC The return filing process is completed only after successful verification. Major Changes in ITR-4 Form from AY 2026-27 CBDT has introduced several significant changes in the ITR-4 form for AY 2026-27 to improve disclosure and tax transparency. 1. Mandatory Bank Balance Disclosure One of the biggest changes is the mandatory disclosure of bank balance under new field E21 in ITR-4. Taxpayers are now required to report the closing balance of business bank accounts as on 31 March 2026. Earlier, reporting of bank balances was optional, but now it has become compulsory for taxpayers opting for presumptive taxation schemes. This change mainly impacts: Section 44AD taxpayers Section 44ADA professionals Section 44AE transport businesses The government introduced this requirement to improve financial transparency and reduce mismatches in income reporting. 2. LTCG Reporting Allowed in ITR-4 Taxpayers can now report Long-Term Capital Gains under Section 112A in ITR-4 if: LTCG does not exceed ₹1.25 lakh No carry forward or set-off of capital losses exists This change benefits small investors who previously had to shift to ITR-2 even for small equity mutual fund gains. 3. Reporting of Two House Properties Earlier, ITR-4 allowed reporting of only one house property. Now taxpayers can disclose income from up to two house properties in the updated form. 4. Additional Disclosure for New Tax Regime The new tax regime under Section 115BAC continues as the default tax regime. Taxpayers opting out of the new regime must now provide: Form 10-IEA acknowledgement details Confirmation regarding continuation or withdrawal from old regime option 5. More Detailed Deduction Reporting Tax deductions under Sections 80C to 80U now require more detailed reporting. Taxpayers must select the appropriate deduction category from dropdown options and mention specific clauses where applicable. 6. Aadhaar Enrolment ID Removed The updated ITR-4 form no longer accepts Aadhaar Enrolment ID. Only a valid 12-digit Aadhaar Number can now be used while filing returns. 7. Additional TDS Reporting Column A new column has been added in the Schedule TDS section to mention the section under which TDS has been deducted. Conclusion The ITR-4 form for AY 2026-27 includes several important updates that taxpayers should understand before filing their returns. Mandatory bank balance disclosure, LTCG reporting facility, detailed deduction disclosures, and revised tax regime reporting are some of the major changes introduced by CBDT. These amendments aim to improve transparency, simplify return filing for small taxpayers, and strengthen compliance monitoring. Taxpayers opting for presumptive taxation schemes under Sections 44AD, 44ADA, and 44AE should carefully review the updated ITR-4 requirements and keep all financial information ready before filing the return. Filing the correct ITR form within the due date and providing accurate disclosures can help taxpayers avoid notices, penalties, and unnecessary complications in future tax assessments.

Reports presumptive business or professional income under Sections 44AD, 44ADA, and 44AE.

Contains details of Tax Deducted at Source (TDS) and Tax Collected at Source (TCS).

Includes details of debtors, creditors, inventory, cash balance, and bank balance.

Taxpayers must disclose all active bank accounts and choose one account for receiving tax refunds.