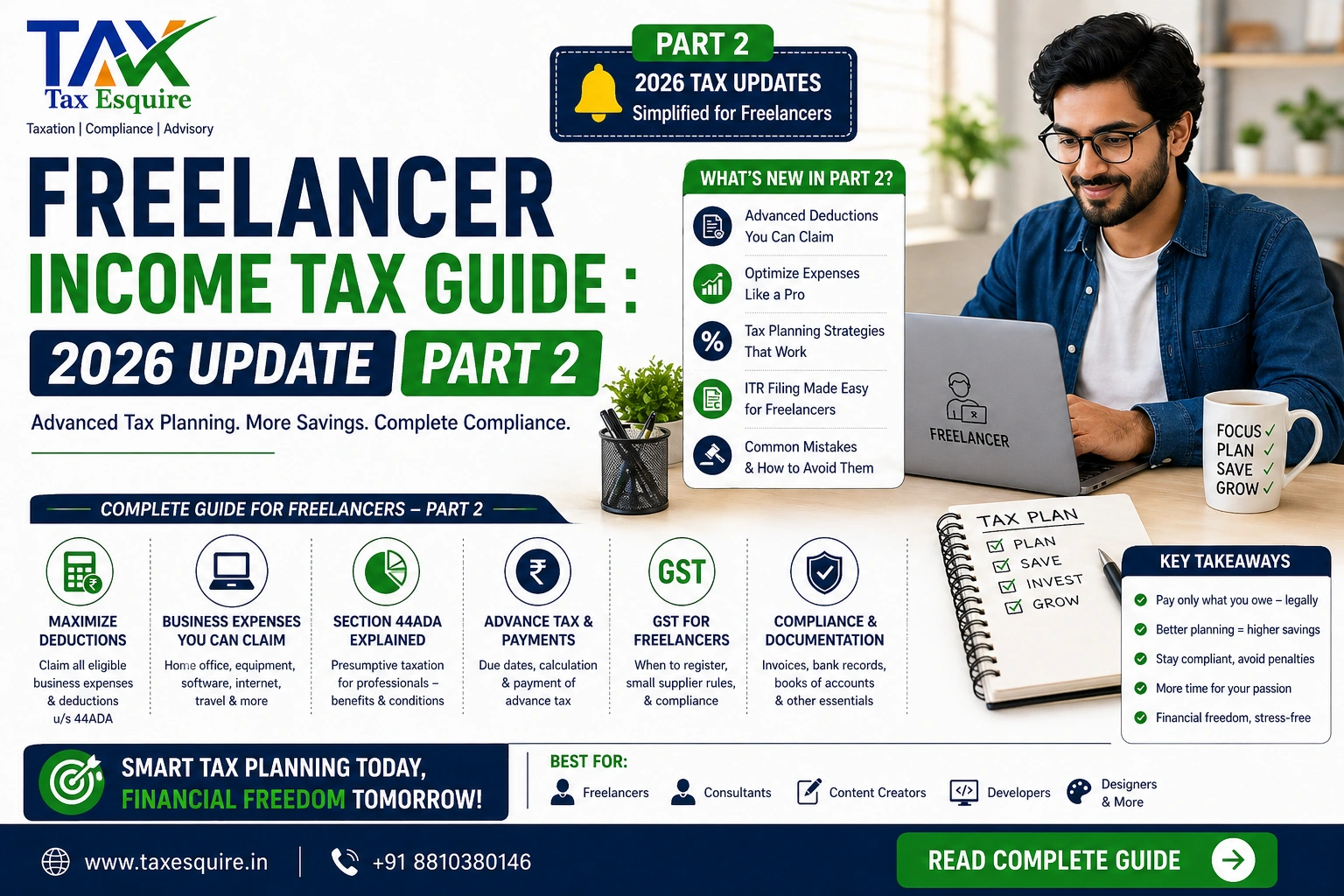

Section 44AD & 44ADA Updated Guide with New Compliance Rules – Part - 2

Benefits of Section 44AD & 44ADA

Presumptive taxation under Sections 44AD and 44ADA is designed to make tax compliance simple, predictable, and cost-effective for small businesses and professionals. Below is a deeper look at how these benefits work in real life:

1. No Complex Accounting

Under normal taxation, taxpayers are required to maintain detailed books of accounts, cash book, ledger, expense records, invoices, and supporting documents. This can be time-consuming and often requires accounting expertise.

With presumptive taxation:

You are not required to maintain detailed books

There is no need to track every expense or justify deductions

Record-keeping becomes minimal and manageable

This is especially helpful for small traders and freelancers who do not have dedicated accounting teams.

2. Reduced Compliance Burden

Tax laws in India involve multiple layers of compliance books of accounts, audit requirements, detailed income calculations, and reconciliations.

Sections 44AD and 44ADA simplify this by:

Eliminating the need for detailed profit calculations

Reducing documentation requirements

Removing the need for audit (in most cases)

As a result, taxpayers can focus more on running their business or profession rather than dealing with complex tax procedures.

3. Lower Professional Costs

Under the normal taxation system, many taxpayers rely on Chartered Accountants for:

Maintaining books

Preparing financial statements

Conducting tax audits

Filing detailed returns

These services can be costly.

With presumptive taxation:

The need for professional assistance is significantly reduced

Compliance becomes simpler, lowering dependency on experts

This leads to direct savings in accounting and audit fees, which is a major advantage for small taxpayers.

4. Quick and Easy Return Filing

Filing income tax returns under normal provisions can be complicated due to:

Detailed income computation

Expense categorization

Balance sheet and profit & loss statements

Under Sections 44AD and 44ADA:

Income is declared at a fixed percentage

Filing is done using ITR-4 (Sugam), which is much simpler

The overall process is faster and less stressful

Even first-time taxpayers can handle filing more confidently with basic guidance.

5. Lower Chances of Scrutiny

When income is calculated based on actual profits, discrepancies or aggressive deductions can trigger scrutiny by the Income Tax Department.

Presumptive taxation reduces this risk because:

Income is declared at standardized rates

There is less scope for manipulation of expenses

Compliance appears more consistent and straightforward

While scrutiny is never completely eliminated, the chances are comparatively lower when rules are properly followed and income matches reported data (like AIS and GST).

Limitations & Risks

Despite the simplicity, there are important drawbacks:

You cannot claim actual expenses

You may pay higher tax than actual profit

Switching rules are restrictive

Mismatch with AIS/GST can trigger notices

Reality check: Presumptive taxation is not always the cheapest option—it is the simplest option.

Practical Examples & Case Studies

Case 1: Small Trader

Turnover: ₹60 lakh

Income declared @6% = ₹3.6 lakh

Even if actual profit is ₹2 lakh, tax will be calculated on ₹3.6 lakh.

Case 2: Freelancer

Receipts: ₹30 lakh

Income declared @50% = ₹15 lakh

If actual expenses are high, this may increase tax liability.

Key Insight

Always compare:

Presumptive income vs Actual income

before making a decision.

Common Mistakes to Avoid

Selecting wrong section

Ignoring the 5-year rule

Declaring unrealistically low turnover

Not checking AIS data

Missing advance tax deadline

These mistakes often lead to notices and penalties.

Who Should Opt for 44AD or 44ADA?

Best suited for:

Small traders with stable margins

Freelancers with predictable income

Those who want simple compliance

Not suitable for:

Low-margin businesses

High-expense professionals

Rapidly growing startups

Choosing wisely can make a huge difference in tax liability.

Step-by-Step Guide to Filing ITR-4 (Sugam)

Filing under presumptive scheme is relatively simple:

Login to Income Tax Portal

Select ITR-4 (Sugam)

Enter turnover or receipts

Declare presumptive income

Add tax details and verify

Submit and e-verify

Expert Tips for Tax Saving & Compliance

Use digital transactions to reduce tax rate

Compare schemes before opting

Pay advance tax on time

Keep basic records even if not required

Seek professional advice for fluctuating income

Smart planning ensures:

Lower tax

Better compliance

Peace of mind

Conclusion

Section 44AD and 44ADA are powerful tool’s for simplifying taxation, but they must be used carefully and strategically.

With increased digital monitoring and stricter compliance rules, taxpayers must:

Stay accurate

Stay consistent

Stay informed

The right approach is not just about saving tax but about avoiding future problem’s while staying compliant.

For prior information, please read ' Section 44AD & 44ADA Updated Guide with New Compliance Rules '. - Click Here