GST Rule 86B: Effective GST Compliance Strategy

Overview

As the dynamics of GST compliance have evolved, Rule 86B vide Notification No. 94/2020 – Central Tax dated 22.12.2020, as part of the CGST (Fourteenth Amendment) Rules, 2020, effective from 01.01.2021. has proved to be a vital regulation that plays an important role in the manner in which Input Tax Credits (ITC) are applied. It guarantees that all taxpayers pay some part of their tax dues in cash instead of availing of full ITC.

Reason for Introducing Rule 86B

Prior to the introduction of Rule 86B, companies were availing ITC as an entire deduction to reduce tax liability, resulting in instances of artificial invoicing and false claims on ITC. In order to prevent these activities, the government implemented this rule so that there would be a genuine inflow of money into the system.

In simpler words: Despite having enough ITC, you are still required to pay a minimum of 1% tax in cash (under certain circumstances).

What is Rule 86B?

Rule 86B of the CGST Rules is an important compliance provision introduced to restrict excessive utilisation of Input Tax Credit (ITC). Under GST, taxpayers are generally allowed to discharge their output tax liability using ITC available in their electronic credit ledger. A registered person is not allowed to use ITC to discharge more than 99% of the output tax liability in a month where-

● The value of taxable supply (excluding exempt and zero-rated supplies) exceeds Rs 50 lakhs.

● This effectively means that at least 1% of the output tax liability must be paid in cash through the electronic cash ledger.

Applicability of Rule 86B

Rule 86B applies to registered persons under the GST regime whose taxable value of supplies (excluding exempt and zero-rated supplies) exceeds ₹50 lakh in a particular month. It is crucial for businesses to assess their taxable turnover monthly before filing GST returns to determine if they fall under this rule. Rule 86B is attached with a non-obstante clause. This implies that this rule overrides all other rules of GST from the date of its enforcement, i.e. 1st January 2021. This rule is applied under the following conditions –

● The rule applies to GST registered businesses whose goods in a month have more than 50 lakhs taxable value.

● The taxable turnover will be exclusive of exempt and zero-rated supply.

● A person should check the value of their goods each month while filing their GST returns.

● The taxable turnover can be calculated as - Taxable turnover = Total turnover of the person - (Zero rated + exempted turnover)

Core Concept of Rule 86B

The application of Rule 86B is limited to using ITC towards paying tax liability:

1. ITC cannot be claimed beyond 99% of tax liability

2. At least 1% must be settled in cash

3. Taxable turnover exceeds ₹50 lakh per month

This is applicable only during the use of ITC, not during its claim.

Points to Consider:

Reverse Charge Mechanism (RCM): Transactions that occur via the RCM process cannot be included as a component of the output tax liability in the computation of the 1% cash payment.

Turnover: The figure of ₹50 lakh will be computed monthly and not on a cumulative basis from past month turnovers.

Zero-Rated Supplies: Although zero-rated supplies are not included when computing the 50 lakh limit, the 1% cash payment is calculated based on the entire output tax liability inclusive of supplies with tax payment.

Applicability of Restriction :-

The applicability of restriction is there in case value of taxable supply exceeds Rs. 50 Lakhs during a particular month

♦ For instance, if in the month of April, 2021, the value of taxable supplies exceeds Rs. 50 Lakhs then only the rule shall apply. In case next month, that is May, 2021, the value of taxable supply doesn’t exceed Rs. 50 Lakhs, the rule won’t apply at all.

Meaning of value of taxable supplies : - As per section 2(108), value of taxable supplies means a supply of goods and/or services that is subject to taxation.

♦ Therefore, in other words, it includes any supply for which charge is made as per sections 9 of CGST or 5 of IGST.

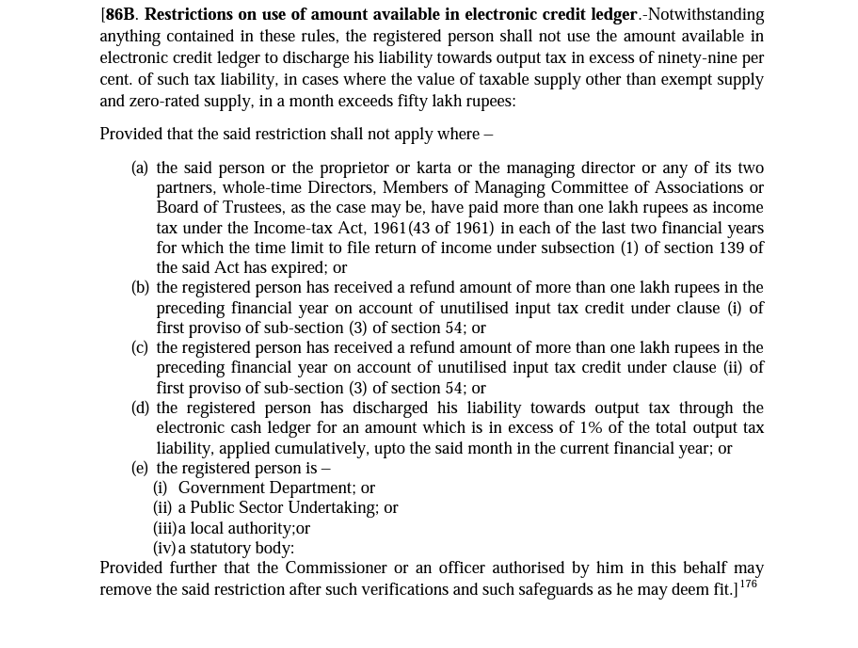

Exceptions to Rule 86B

While Rule 86B applies broadly, certain exceptions allow specific taxpayers to bypass these restrictions:

1. High Income Tax Payments: If a registered person or their key stakeholders (proprietor/karta/managing director/partners) have paid income tax exceeding ₹1 lakh in each of the preceding two financial years, they are exempt from this rule.

2. Refund Recipients: Registered persons who received a refund greater than ₹1 lakh in the previous financial year due to exports under LUT or an inverted tax structure are also exempt.

3. Excess Cash Payments: If a registered person has discharged their output tax liability by electronic cash ledger for an amount exceeding 1% cumulatively during the current financial year, they may be exempt.

4. Government Bodies: Statutory bodies such as government departments, public sector undertakings, local authorities, and statutory authorities are not subject to the restrictions imposed by Rule 86B.

5. Discretionary Powers of Commissioner: The Commissioner or authorized officials can remove restrictions on a case-by-case basis after due verification.

Key Restrictions Imposed by Rule 86B

Under Rule 86B, applicable registered persons cannot utilize ITC exceeding 99% of their total output tax liability. In simpler terms, businesses with a monthly taxable turnover above ₹50 lakh are required to pay at least 1% of their output tax liability in cash. This restriction effectively limits the usage of ITC accumulated through purchases.

Illustration – Impact of Rule 86B (Restriction on ITC Utilisation)

Assumptions: Consider a firm which is having ITC Balance: High and Cash Balance: Low

• Output Tax Liability: ₹18,00,000

• ITC Available in E-Credit Ledger: ₹20,00,000

• Auto-populated ITC (GSTR-2B): ₹20,00,000

Pre-Amendment Scenario (Before Rule 86B)

• The taxpayer could utilise entire ITC available in the electronic credit ledger.

• ITC utilised = ₹18,00,000

• Balance tax payable in cash = Nil

Post-Amendment Scenario (After Rule 86B – 99% ITC Restriction)

• Maximum ITC utilisation allowed = 99% of output tax liability

=₹18,00,000 × 99% = ₹17,82,000

• However, ITC available = ₹20,00,000 (Higher than limit)

• Therefore, ITC utilised = ₹17,82,000

• Mandatory minimum cash payment (1%)

=₹18,00,000 × 1% = ₹18,000

• Total cash payable = ₹18,000

(₹18,000 mandatory)

• Remaining ITC balance = ₹2,18,000

(₹20,00,000 – ₹17,82,000)

Impact of Rule 86B on Businesses

Rule 86B’s Impact in particular, appears to be targeted at large taxpayers with relatively higher taxable turnover, and therefore, its effect on micro and small businesses is not as likely. The primary objective of the rule is to reduce the practice of issuing fake invoices and using the same for ITC purposes to avoid tax payments.

In this regard, among other things, it requires a minimum cash payment of 1% so as to show genuine transactions rather than merely claiming ITCs to meet their tax obligations.

In the case of bigger businesses, however, this will lead to the management of working capital and cash flows. For those that are heavily reliant on ITCs, their tax obligation will be substantially reduced.

Rule 86 B is an important rule within the GST regime intended to avoid the abuse of ITC and maintain the minimum requirement of cash payment. Even as it places limitations, it offers several exceptions and relief options.

Practical Insight for Taxpayers By TaxEsquire

While Form 121 helps in preventing unnecessary TDS deductions, it does not exempt income from tax. If the total income later exceeds the exemption limit, the taxpayer is still required to disclose such income and pay tax while filing the return.

From a compliance perspective, taxpayers should ensure:

• Accurate estimation of annual income

• Timely submission to each payer separately

• Consistency with income reported in ITR

Author: CA POONAM GUPTA & ADV LOKESH GUPTA

© 2026 Tax Esquire | Expert CA Services in Greater Noida, Uttar Pradesh

8810380146 | info.taxesquire@gmail.com | taxesquire.in

This document is for informational purposes only. For personalised tax advice, consult our chartered accountants.