Audit Compliance for Private Limited Companies in India

After incorporating a private limited company in India, compliance does not end with registration. In fact, incorporation is just the beginning of a company’s legal and regulatory responsibilitie’s. Every company is required to follow a series of compliance’s prescribed under the Companies Act, 2013, and one of the most important among them is the requirement to conduct audit’s.

Audit compliance is not dependent on the size, turnover, or profitability of the business. Even if a company has not commenced operations or is incurring losses, it is still legally required to get its account’s audited. This make’s auditing a fundamental compliance obligation for every private limited company.

A company audit represents an in-depth review and verification of the financial records of a company. In order to demonstrate the accuracy, completeness, and compliance with the law and accounting standards of the financial records, each company shall have a qualified, independent auditor form an opinion regarding whether the financial statements accurately and fairly present the financial condition of the company.

During the audit process, the auditor carefully examine’s variou’s financial document’s such as books of account’s, invoice’s, voucher’s, bill’s, bank statement’s, and supporting record’s. This verification process help’s in identifying discrepancie’s, ensuring compliance, and strengthening financial discipline within the organization. The audit of a private limited company is an annual requirement under the Act and the relevant Company Law Rules, making it an essential part of corporate governance.

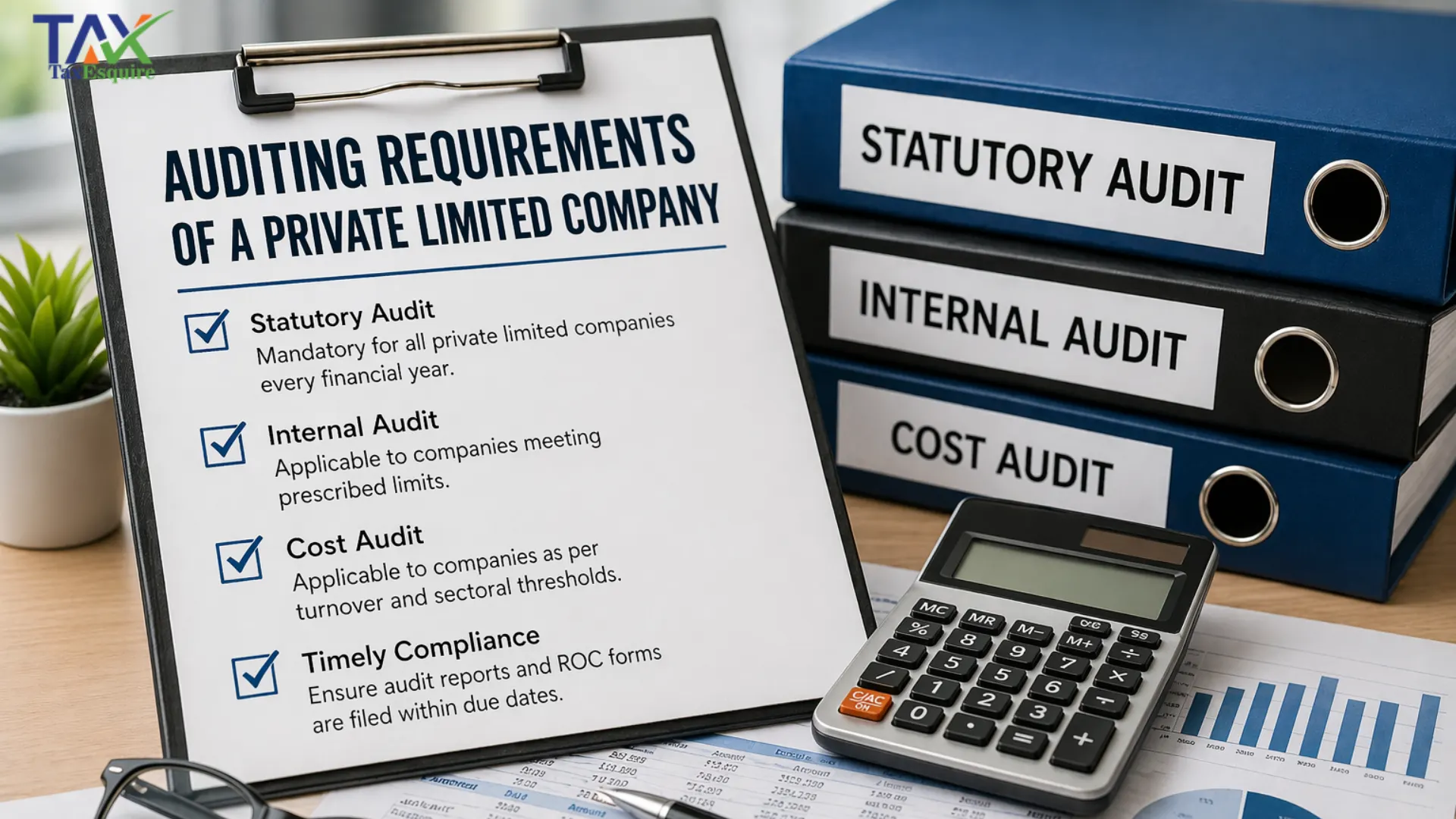

There are different type’s of audits applicable to private limited companie’s, each serving a specific purpose. While some audits are mandatory for all companie’s, other’s are applicable only when certain condition’s or thresholds are met. Understanding these audits helps businesses stay compliant and manage their financial system’s more effectively.

Statutory Audit

A statutory audit is the most important and compulsory audit for every private limited company. It is mandated by law and must be conducted annually, irrespective of whether the company is earning profit’s or running at a loss. This means that even dormant companie’s or newly incorporated entitie’s are required to undergo statutory audits.

The statutory audit is conducted in accordance with the provisions of the Companies Act and the Companies (Accounts) Rules, 2014. The primary objective of this audit is to determine whether the financial statements prepared by the company present a true and fair view of its financial performance and position.

The auditor perform’s a detailed examination of financial record’s, including balance sheet’s, profit and loss statements, cash flow statement’s, and supporting document’s. They also verify bank balances, transactions, and accounting practice’s followed by the company. Based on this examination, the auditor issues an audit report expressing an independent opinion.

Statutory audits play a crucial role in maintaining transparency and accountability. They not only help in detecting errors or fraud but also enhance the credibility of the company in the eyes of investor’s, lender’s, and regulatory authorities.

Internal Audit

Internal audit is not universally mandatory for all private limited companie’s, but it becomes applicable when certain financial thresholds are met. Unlike statutory audit, which focuses on compliance, internal audit is more focused on improving the internal functioning of the company.

As per the Companies Act and the Companies (Accounts) Rules, 2014, internal audit is required for specified private companies, such as:

Companies having a turnover of ₹200 crore or more during the previous financial year

Companies having outstanding loans or borrowings from banks or public financial institutions exceeding ₹100 crore

The objective of an internal audit is to evaluate the effectiveness of internal controls, risk management system’s, and operational processes. It involves a continuous review of financial and non-financial activitie’s to ensure that the company is functioning efficiently.

Internal audits provide valuable insight’s to management by identifying weaknesses in systems, highlighting inefficiencie’s, and suggesting improvemen’ts. This enables the company to take corrective actions proactively and strengthen its overall governance framework.

Cost Audit

Cost audit is a specialized type of audit applicable to companie’s engaged in specific industrie’s, particularly manufacturing and certain service sectors. It is governed by the Companies Rule’s, 2014 and is applicable only when prescribed turnover thresholds are met.

The applicability of cost audit depend’s on the nature of business and turnover limit’s. For companies covered under Table 3(A), cost audit becomes applicable when:

The overall turnover is ₹50 crore or more, and

The turnover of the individual product or service is ₹25 crore or more

For companies covered under Table 3(B), the thresholds are higher:

Overall turnover of ₹100 crore or more, and

Product or service turnover of ₹35 crore or more

The purpose of a cost audit is to verify the cost records maintained by the company and ensure that they are accurate and in line with prescribed standards. It also helps in analyzing cost efficiency, pricing strategie’s, and resource utilization.

Cost audits are particularly important for industrie’s where cost control directly impact’s profitability and competitiveness. They provide management with insights into cost structure’s and help in making informed business decisions.

Appointment of an Auditor

The appointment of auditors is a critical step in ensuring proper audit compliance. Different types of audits require different types of auditors, and specific timelines must be followed for their appointment.

Statutory Auditor

Every private limited company is required to appoint its first statutory auditor within 30 days from the date of incorporation. This initial appointment is generally made by the Board of Directors. Thereafter, the appointment is confirmed by the shareholder’s at the first Annual General Meeting (AGM).

Once appointed, the statutory auditor hold’s office for a term of five years, subject to compliance with applicable provision’s. The auditor must be an independent practising Chartered Accountant, a CA firm, or an LLP where the majority of partners are practising in India.

The independence of the statutory auditor is essential to ensure unbiased reporting and maintain the integrity of the audit process.

Internal Auditor

The appointment of an internal auditor is decided by the Board of Directors based on the applicability criteria. The company has flexibility in choosing the internal auditor, who can be:

A Chartered Accountant

A Cost Accountant

Any other qualified professional

Even an internal employee of the company

This flexibility allows companies to design their internal audit function according to their operational needs and complexity.

Cost Auditor

Companies that are required to conduct cost audit’s must appoint a cost auditor within 180 days from the commencement of the financial year. The cost auditor must be a cost accountant in practice, as defined under the Cost and Works Accountants Act, 1959.

The appointment of a qualified cost auditor ensures that cost records are examined by a professional with specialized knowledge in cost accounting and analysis.

Due Date of Private Limited Company Audit

Timely completion of audits and filing of related document’s is essential to avoid penalties and ensure compliance with regulatory requirement’s.

Statutory Audit

The statutory audit must be completed before the Annual General Meeting of the company. The auditor is required to submit the audit report to the Board of Directors before the AGM is held. This report is then attached to the company’s financial statement’s.

The key due dates are as follows:

AGM must be held on or before 30th September each year

Form AOC-4 must be filed within 30 days of the AGM

Form MGT-7 must be filed within 60 days of the AGM

These filings are made with the Registrar of Companies (ROC) and are essential for maintaining the company’s compliance status.

Internal Audit

There is no specific statutory due date prescribed for conducting internal audit’s. However, the internal auditor is expected to submit the audit report to the Board before the AGM so that it can be considered along with the financial statement’s.

The findings of the internal audit may also be included in the overall reporting and compliance framework of the company.

Cost Audit

The cost audit report must be submitted to the Board of Director’s by 30th September each year in the prescribed format (CRA-3). After reviewing the report, the Board is required to file it with the Central Government within 30 days using Form CRA-4.

Timely submission and filing of cost audit report’s are crucial to ensure compliance with cost audit regulation’s.

ROC Forms for Audit Requirements

Private limited companie’s are required to file several form’s with the ROC in relation to audit compliance. Each form serves a specific purpose and must be filed within the prescribed timeline’s.

Proper and timely filing of these forms ensures that the company remains compliant with regulatory requirements and avoids unnecessary legal complications.

Consequences of Non-Compliance

Failure to comply with audit requirement’s or delay in filing the necessary forms can result in penalties and legal consequence’s for the company and its directors. Non compliance may also affect the company’s reputation and credibility in the market.

In addition to financial penaltie’s, companie’s may face difficulties in raising fund’s, obtaining loans, or entering into business agreement’s if their compliance status is not up to date. Therefore, maintaining proper audit compliance is essential for the smooth functioning and growth of the business.

Why Choose TaxEsquire?

At TaxEsquire, we go beyond just compliance—we provide strategic financial guidance to help your business grow.

Our Expertise Includes:

- • Statutory Audit & Compliance

• Internal & Risk Audit

• ROC Filing & Annual Compliance

• GST & Income Tax Advisory

• Startup & Business Consulting

Conclusion

Audit is not just a legal formality it is a foundation for financial discipline and business credibility. Every Private Limited Company must treat audit compliance as a priority to avoid penaltie’s and build long term trust.

Partnering with the right professional’s ensure’s that your company remain’s compliant, efficient, and growth ready

Author: CA POONAM GUPTA & ADV LOKESH GUPTA

Companies having a turnover of ₹200 crore or more during the previous financial year

Companies having outstanding loans or borrowings from banks or public financial institutions exceeding ₹100 crore

The overall turnover is ₹50 crore or more, and

The turnover of the individual product or service is ₹25 crore or more

Overall turnover of ₹100 crore or more, and

Product or service turnover of ₹35 crore or more

The purpose of a cost audit is to verify the cost records maintained by the company and ensure that they are accurate and in line with prescribed standards. It also helps in analyzing cost efficiency, pricing strategie’s, and resource utilization.

Appointment of an Auditor

A Chartered Accountant

A Cost Accountant

Any other qualified professional

Even an internal employee of the company

AGM must be held on or before 30th September each year

Form AOC-4 must be filed within 30 days of the AGM

Form MGT-7 must be filed within 60 days of the AGM

Why Choose TaxEsquire?

• Internal & Risk Audit

• ROC Filing & Annual Compliance

• GST & Income Tax Advisory

• Startup & Business Consulting

Conclusion

© 2026 Tax Esquire | Expert CA Services in Greater Noida, Uttar Pradesh

8810380146 | info.taxesquire@gmail.com | taxesquire.in

This document is for informational purposes only. For personalised tax advice, consult our chartered accountants.