GST Audit Under Section 65 & 66: Departmental vs Special Audit

Introduction

The Goods and Services Tax (GST) system has transformed India’s indirect taxation landscape by introducing transparency, digitization, and uniformity. However, with increased compliance requirements and real-time data tracking, businesses must ensure that their GST filings are accurate and consistent.

A GST audit plays a crucial role in this ecosystem. It acts as a verification mechanism to ensure that businesses correctly report their financial data, tax liabilities, and input tax credit claims.

In 2026, GST audits are no longer limited to traditional checks. Authorities now use data analytics, AI-based scrutiny, and system-driven reconciliation to identify discrepancies. Therefore, businesses must shift from reactive compliance to proactive audit preparedness.

What is GST Audit under GST Law?

A GST audit refers to the systematic examination of a taxpayer’s records, returns, and financial statements to verify compliance with GST laws. The audit ensures that all transactions are correctly recorded and taxes are appropriately paid.

Key Objectives of GST Audit:

● To verify the correctness of declared turnover

● To ensure accurate tax payment and liability calculation

● To validate Input Tax Credit (ITC) claims

● To detect errors, fraud, or tax evasion

Unlike earlier tax regimes, GST audits rely heavily on data matching across multiple returns, such as GSTR-1, GSTR-3B, and GSTR-2B.

Legal Framework & Recent Amendments

GST audit provisions are primarily governed by the Central Goods and Services Tax (CGST) Act, 2017.

Relevant Sections:

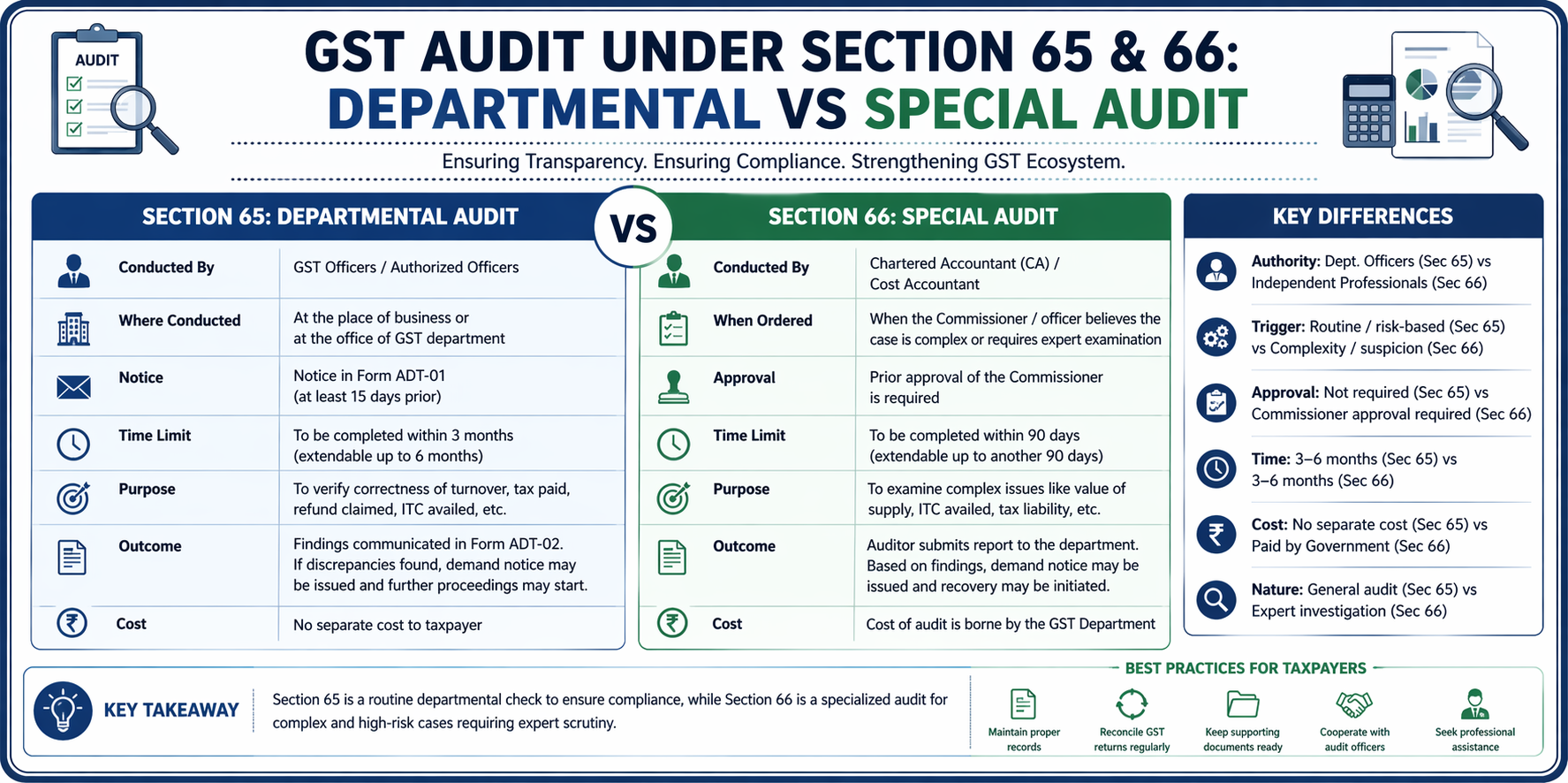

● Section 65 – Audit by tax authorities

● Section 66 – Special audit

Recent Amendments:

● The requirement for mandatory GST audit by a Chartered Accountant or Cost Accountant based on turnover has been removed.

● Taxpayers now file self-certified reconciliation statements (GSTR-9C).

● Authorities increasingly rely on automated scrutiny and risk-based selection for audits.

This shift means that businesses must maintain accurate records at all times, as audits can be triggered without prior pattern.

Applicability of GST Audit (Latest Rules)

Earlier, businesses exceeding a specific turnover threshold were required to undergo a GST audit. However, the law has evolved.

Current Applicability:

● Departmental Audit: Selected by GST authorities based on risk parameters

● Special Audit: Ordered in complex or suspicious cases

● Voluntary/Internal Audit: Conducted by businesses for compliance

Although mandatory audit has been removed, scrutiny has increased significantly, making compliance even more critical.

Threshold Limits & Turnover Calculation

Even though GST audit is no longer turnover-based, calculating aggregate turnover remains essential for compliance and reporting.

Aggregate Turnover Includes:

● Taxable supplies

● Exempt supplies

● Exports

● Interstate supplies

Excludes:

● GST taxes (CGST, SGST, IGST)

● Inward supplies under reverse charge

Practical Example:

If a business has:

● ₹1 crore taxable supply

● ₹20 lakh exempt supply

● ₹30 lakh export

Aggregate turnover = ₹1.5 crore

Accurate turnover calculation is crucial for return filing, reconciliation, and avoiding notices.

Types of GST Audit

1. Departmental Audit (Section 65): This audit is conducted by GST officers to verify compliance. It is typically initiated based on risk profiling.

2. Special Audit (Section 66): This is ordered when authorities find discrepancies or complexity in records. It is conducted by a nominated CA or CMA.

3. Internal GST Audit (Recommended): Businesses often conduct internal audits to identify errors before authorities do. This is a best practice for risk management.

GST Audit Process (Step-by-Step)

The GST audit process involves multiple stages:

Step 1: Notice Issuance: Authorities issue a notice informing the taxpayer about the audit.

Step 2: Document Submission: The taxpayer must provide financial records, GST returns, and supporting documents.

Step 3: Verification & Reconciliation: Auditors compare GST returns with books of accounts and external data.

Step 4: Query Handling: Authorities may raise queries for clarification on discrepancies.

Step 5: Audit Report: A final report is prepared highlighting findings.

Step 6: Compliance Action: Taxpayers must rectify errors, pay additional tax, or respond to notices.

GST Audit Timelines & Deadlines

● Departmental audit must be completed within 3 months, extendable up to 6 months

● Annual return (GSTR-9) deadlines must be adhered to

● Delayed compliance may trigger scrutiny or penalties

Timely filing and reconciliation are essential to avoid audit complications.

Documents Required for GST Audit

A GST audit requires comprehensive documentation:

● GST returns (GSTR-1, GSTR-3B, GSTR-9)

● Financial statements (Balance Sheet, P&L)

● Purchase and sales registers

● ITC records and invoices

● E-invoices and e-way bills

● Bank statements

● Contracts and agreements

Proper documentation ensures a smooth audit process and reduces risk.

Detailed GST Audit Checklist (Practical Section)

1 Registration & Basic Details Verification: Ensure GST registration details are correct and updated.

2 Returns & Reconciliation: Match GSTR-1, GSTR-3B, and books of accounts to identify mismatches.

3 Outward Supply Verification: Verify correct classification of supplies and tax rates applied.

4 Input Tax Credit (ITC) Check: Check eligibility, matching with GSTR-2B, and blocked credits.

5 Reverse Charge Mechanism (RCM): Ensure correct identification and reporting of RCM transactions.

6 E-Invoice & E-Way Bill Compliance: Verify compliance with e-invoicing rules and e-way bill generation.

7 Export & Zero-Rated Supplies: Check LUT compliance and refund claims.

8 Turnover & Financial Reconciliation: Ensure consistency between GST returns and financial statements.

GST Audit by Department (Section 65)

● Conducted by GST authorities

● Prior notice is issued

● Can be conducted at business premises

● Focuses on compliance gaps

Special Audit under GST (Section 66)

● Ordered in complex cases

● Conducted by CA/CMA

● Cost borne by government

● Used when discrepancies are significant

Common GST Audit Issues & Errors

● ITC mismatch with GSTR-2B

● Incorrect tax classification

● Turnover discrepancies

● Missing invoices

● Reconciliation errors

Practical Issues & Challenges in GST Audit

● Data mismatch between systems

● Frequent law changes

● Poor documentation practices

● ERP vs GST portal differences

Penalties & Consequences of Non-Compliance

Non-compliance can lead to:

● Interest on unpaid tax

● Financial penalties

● GST notices and litigation

● ITC reversal

Benefits of GST Audit for Businesses

● Improved compliance

● Reduced risk of penalties

● Better financial accuracy

● Enhanced credibility

GST Audit vs Tax Audit vs Annual Return

|

Aspect |

GST Audit |

Tax Audit |

Annual Return |

|

Law |

GST |

Income Tax |

GST |

|

Purpose |

Compliance |

Income verification |

Summary filing |

|

Applicability |

Conditional |

Turnover-based |

Mandatory |

Practical Tips to Prepare for GST Audit

● Perform monthly reconciliation

● Maintain proper records

● Conduct internal audits

● Use accounting software

● Review ITC regularly

Latest Updates & Expert Tips (2026)

● AI-based GST scrutiny is increasing

● Real-time data matching is stricter

● ITC verification is a major focus area

● E-invoicing applicability is expanding

Conclusion

GST audit in 2026 is a continuous compliance process, not a one-time activity. With increasing scrutiny and digital monitoring, businesses must adopt a proactive approach.

Regular reconciliation, proper documentation, and internal audits can help businesses stay compliant, avoid penalties, and build long-term credibility.

© 2026 Tax Esquire | Expert CA Services in Greater Noida, Uttar Pradesh

8810380146 | info.taxesquire@gmail.com | taxesquire.in

This document is for informational purposes only. For personalised tax advice, consult our chartered accountants.