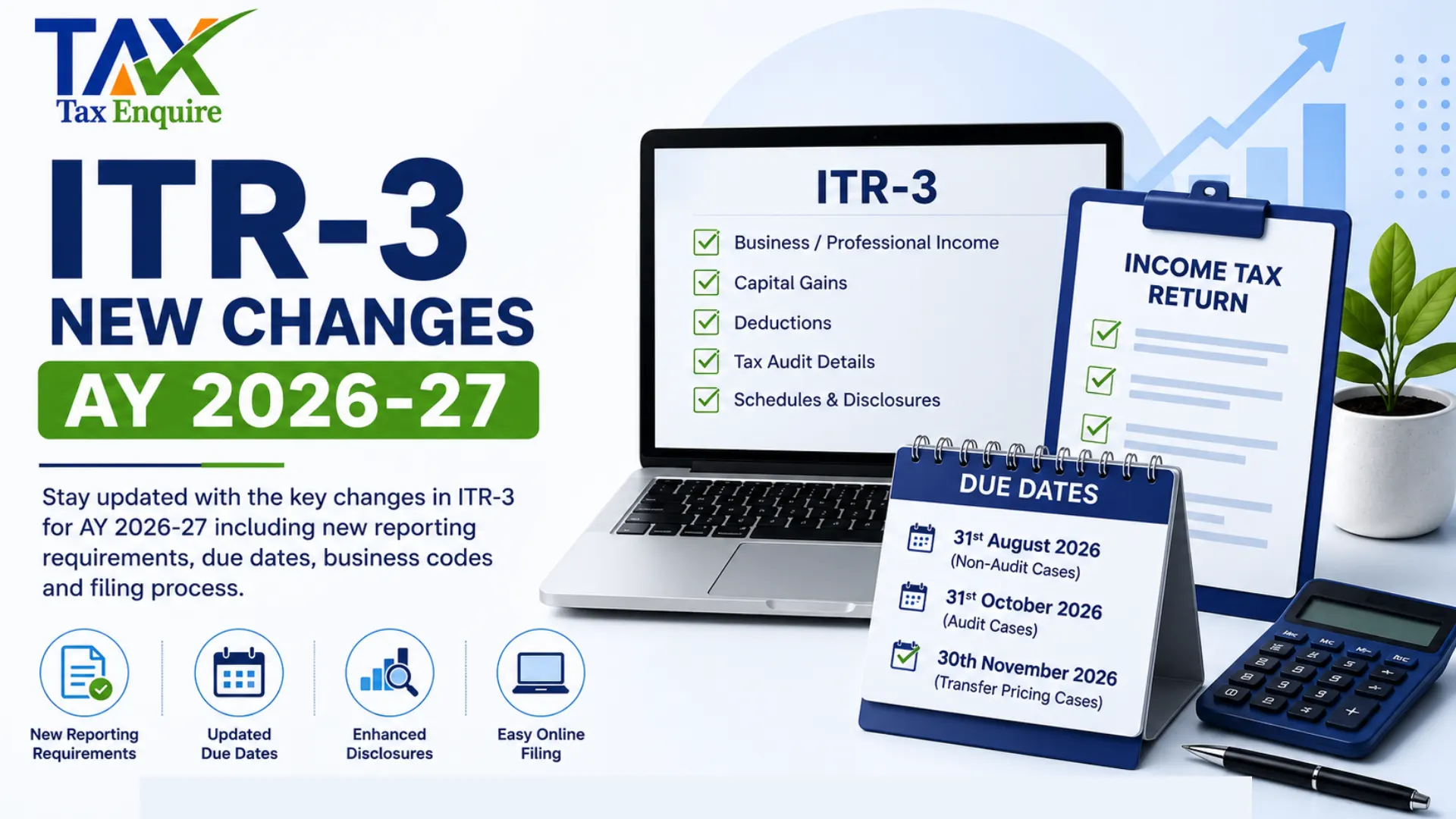

ITR-3 New Changes AY 2026-27

Introduction

The Income Tax Department has introduced several important updates in the ITR-3 form for Assessment Year (AY) 2026-27. These changes mainly affect business owners, professionals, freelancers, stock market traders, consultants, and taxpayers earning income from proprietary business or profession. The revised ITR-3 form focuses on better transparency, detailed disclosure requirements, and improved reporting accuracy for different types of income.

Eligibility Criteria for Filing ITR-3

ITR-3 can be filed by Individuals and Hindu Undivided Families (HUFs) having income from business or profession. The following taxpayers are generally eligible to file ITR-3:

Proprietors carrying on business or profession

Freelancers and consultants

Doctors, lawyers, architects, chartered accountants, and other professionals

Taxpayers having income from F&O trading, intraday trading, or share trading

Partners receiving remuneration or interest from partnership firms

Taxpayers opting for presumptive taxation in certain cases

Individuals having business income along with salary, house property, capital gains, or income from other sources

Who is Not Eligible to File ITR-3?

The following persons cannot file ITR-3:

Companies, LLPs, and partnership firms

Individuals not having business or professional income

Taxpayers eligible to file ITR-1, ITR-2, or ITR-4

Salaried individuals without business income

Major New Changes in ITR-3 for AY 2026-27

1. Separate Disclosure for F&O and Intraday Trading

The updated ITR-3 form now requires separate reporting for:

Futures & Options (F&O) turnover

Intraday trading turnover

Speculative business income

This change improves reporting accuracy for stock market traders and investors.

2. Additional Deduction Reporting

Enhanced disclosure requirements have been introduced for deductions claimed under:

Section 80G

Section 80GGC

Section 80DD

Section 80U

Taxpayers may need to provide more details while claiming deductions.

3. Capital Gains Reporting Simplified

The earlier requirement of bifurcating capital gains before and after 23rd July 2024 has been simplified in the revised ITR forms. This reduces complexity for taxpayers reporting capital gains transactions.

4. Expanded Crypto Reporting

Taxpayers dealing in cryptocurrencies and Virtual Digital Assets (VDAs) may now need to provide more detailed disclosures in ITR-3.

5. New Business Codes Added

Several new business and profession codes have been introduced for:

Social media influencers

F&O traders

Speculative traders

Share traders

Commission agents

Last Date to File ITR-3 for FY 2025-26

Late filing may result in penalty, interest, and loss of certain benefits such as carry forward of losses.

What is the Structure of ITR-3?

The ITR-3 form consists of multiple sections and schedules for detailed income reporting. Major parts of the form include:

How to File Your ITR-3 Online on Income Tax Portal?

The online filing process for ITR-3 generally includes the following steps:

Visit the Income Tax e-filing portal

Login using PAN and password

Select “File Income Tax Return”

Choose AY 2026-27

Select ITR-3 form

Enter business, professional, salary, and capital gain details

Report deductions and tax payments

Verify tax liability and submit the return

Complete e-verification through Aadhaar OTP, EVC, or net banking

Proper books of accounts, bank statements, GST records, and Form 26AS should be kept ready before filing the return.

Business Codes for ITR Forms

Agriculture, Animal Husbandry & Forestry

Fish Farming Mining & Quarrying Manufacturing Sector Construction Sector Real Estate & Renting Wholesale & Retail Trade Newly Added Business Codes These newly introduced business codes are especially important for traders, influencers, and digital professionals while filing ITR-3 for AY 2026-27. Conclusion The revised ITR-3 form for AY 2026-27 introduces major changes related to trading income disclosure, deduction reporting, business classification, and digital asset reporting. Taxpayers engaged in business or profession should carefully review the updated requirements before filing their returns. Proper disclosure and selection of the correct business code can help avoid notices, defective returns, and tax scrutiny.

Author: CA POONAM GUPTA & ADV LOKESH GUPTA

© 2026 Tax Esquire | Expert CA Services in Greater Noida, Uttar Pradesh

8810380146 | info.taxesquire@gmail.com | taxesquire.in

This document is for informational purposes only. For personalised tax advice, consult our chartered accountants.